Note

-

Download Jupyter notebook:

https://docs.doubleml.org/stable/examples/py_double_ml_cvar.ipynb.

Python: Conditional Value at Risk of potential outcomes#

In this example, we illustrate how the DoubleML package can be used to estimate the conditional Value at Risk of potential outcomes. The estimation is based on Kallus et al. (2019).

Data#

We define a data generating process to create synthetic data to compare the estimates to the true effect.

[1]:

import numpy as np

import pandas as pd

import doubleml as dml

import multiprocessing

from lightgbm import LGBMClassifier, LGBMRegressor

The data is generated as a location-scale model with

where \(X_i\sim\mathcal{U}[-1,1]^{p}\) and \(\varepsilon_i \sim \mathcal{N}(0,1)\). Further, the location and scale are determined according to the following functions

and the treatment takes the following form

with \(\epsilon_i \sim \mathcal{N}(0,1)\).

[2]:

def f_loc(D, X):

loc = 0.5*D + 2*D*X[:,4] + 2.0*(X[:,1] > 0.1) - 1.7*(X[:,0] * X[:,2] > 0) - 3*X[:,3]

return loc

def f_scale(D, X):

scale = np.sqrt(0.5*D + 0.3*D*X[:,1] + 2)

return scale

def dgp(n=200, p=5):

X = np.random.uniform(-1,1,size=[n,p])

D = ((X[:,1 ] - X[:,3] + 1.5*(X[:,0] > 0) + np.random.normal(size=n)) > 0)*1.0

epsilon = np.random.normal(size=n)

Y = f_loc(D, X) + f_scale(D, X)*epsilon

return Y, X, D, epsilon

We can calculate the true conditional value at risk through simulations. Here, we will just approximate the true conditional value at risk for the potential outcomes for a range of quantiles.

[3]:

tau_vec = np.arange(0.1,0.95,0.05)

p = 5

n_true = int(10e+6)

_, X_true, _, epsilon_true = dgp(n=n_true, p = p)

D1 = np.ones(n_true)

D0 = np.zeros(n_true)

Y1 = f_loc(D1, X_true) + f_scale(D1, X_true)*epsilon_true

Y0 = f_loc(D0, X_true) + f_scale(D0, X_true)*epsilon_true

Y1_quant = np.quantile(Y1, q=tau_vec)

Y0_quant = np.quantile(Y0, q=tau_vec)

Y1_cvar = [Y1[Y1 >= quant].mean() for quant in Y1_quant]

Y0_cvar = [Y0[Y0 >= quant].mean() for quant in Y0_quant]

print(f'Conditional Value at Risk Y(0): {Y0_cvar}')

print(f'Conditional Value at Risk Y(1): {Y1_cvar}')

Conditional Value at Risk Y(0): [np.float64(0.5473064979425033), np.float64(0.756585519864526), np.float64(0.9574793755564219), np.float64(1.1539831483813536), np.float64(1.3486970271639334), np.float64(1.5436876323961168), np.float64(1.7407627053044026), np.float64(1.9417090334740552), np.float64(2.1484554868601506), np.float64(2.3631031251500065), np.float64(2.5883964619856044), np.float64(2.827874854703913), np.float64(3.086401570476133), np.float64(3.3711317415516624), np.float64(3.6934117220290754), np.float64(4.0735183279373635), np.float64(4.554986206618521)]

Conditional Value at Risk Y(1): [np.float64(1.1121351274811793), np.float64(1.3466832975109777), np.float64(1.5714294154804167), np.float64(1.7910908091075142), np.float64(2.008825189994473), np.float64(2.227018245501943), np.float64(2.447863428811719), np.float64(2.6734628878523097), np.float64(2.906051023766621), np.float64(3.1482102407485826), np.float64(3.403113188429014), np.float64(3.675011328023803), np.float64(3.969702563412915), np.float64(4.295855642811191), np.float64(4.667285944503316), np.float64(5.108783087402629), np.float64(5.673581815999206)]

Let us generate \(n=5000\) observations and convert them to a DoubleMLData object.

[4]:

n = 5000

np.random.seed(42)

Y, X, D, _ = dgp(n=n,p=p)

obj_dml_data = dml.DoubleMLData.from_arrays(X, Y, D)

Conditional Value at Risk (CVaR)#

Next, we can initialize our two machine learning algorithms to train the different nuisance elements (remark that in contrast to potential quantile estimation ml_g is a regressor). Then we can initialize the DoubleMLCVAR objects and call fit() to estimate the relevant parameters. To obtain confidence intervals, we can use the confint() method.

[5]:

ml_g = LGBMRegressor(n_estimators=300, learning_rate=0.05, num_leaves=10, verbose=-1, n_jobs=1)

ml_m = LGBMClassifier(n_estimators=300, learning_rate=0.05, num_leaves=10, verbose=-1, n_jobs=1)

CVAR_0 = np.full((len(tau_vec)), np.nan)

CVAR_1 = np.full((len(tau_vec)), np.nan)

ci_CVAR_0 = np.full((len(tau_vec),2), np.nan)

ci_CVAR_1 = np.full((len(tau_vec),2), np.nan)

for idx_tau, tau in enumerate(tau_vec):

print(f'Quantile: {tau}')

dml_CVAR_0 = dml.DoubleMLCVAR(obj_dml_data,

ml_g, ml_m,

quantile=tau,

treatment=0,

n_folds=5)

dml_CVAR_1 = dml.DoubleMLCVAR(obj_dml_data,

ml_g, ml_m,

quantile=tau,

treatment=1,

n_folds=5)

dml_CVAR_0.fit()

dml_CVAR_1.fit()

ci_CVAR_0[idx_tau, :] = dml_CVAR_0.confint(level=0.95).to_numpy()

ci_CVAR_1[idx_tau, :] = dml_CVAR_1.confint(level=0.95).to_numpy()

CVAR_0[idx_tau] = dml_CVAR_0.coef.squeeze()

CVAR_1[idx_tau] = dml_CVAR_1.coef.squeeze()

Quantile: 0.1

Quantile: 0.15000000000000002

Quantile: 0.20000000000000004

Quantile: 0.25000000000000006

Quantile: 0.30000000000000004

Quantile: 0.3500000000000001

Quantile: 0.40000000000000013

Quantile: 0.45000000000000007

Quantile: 0.5000000000000001

Quantile: 0.5500000000000002

Quantile: 0.6000000000000002

Quantile: 0.6500000000000001

Quantile: 0.7000000000000002

Quantile: 0.7500000000000002

Quantile: 0.8000000000000002

Quantile: 0.8500000000000002

Quantile: 0.9000000000000002

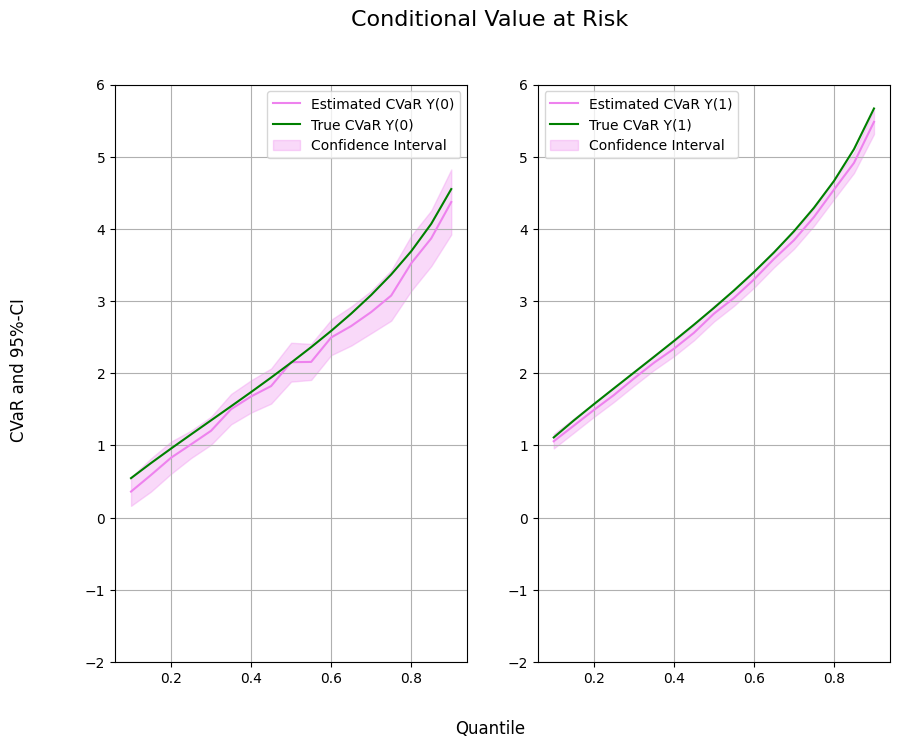

Finally, let us take a look at the estimated values.

[6]:

data = {"Quantile": tau_vec, "CVaR Y(0)": Y0_cvar, "CVaR Y(1)": Y1_cvar,

"DML CVaR Y(0)": CVAR_0, "DML CVaR Y(1)": CVAR_1,

"DML CVaR Y(0) lower": ci_CVAR_0[:, 0], "DML CVaR Y(0) upper": ci_CVAR_0[:, 1],

"DML CVaR Y(1) lower": ci_CVAR_1[:, 0], "DML CVaR Y(1) upper": ci_CVAR_1[:, 1]}

df = pd.DataFrame(data)

print(df)

Quantile CVaR Y(0) CVaR Y(1) DML CVaR Y(0) DML CVaR Y(1) \

0 0.10 0.547306 1.112135 0.360683 1.057962

1 0.15 0.756586 1.346683 0.590911 1.273356

2 0.20 0.957479 1.571429 0.829543 1.489699

3 0.25 1.153983 1.791091 1.015038 1.697000

4 0.30 1.348697 2.008825 1.203284 1.925736

5 0.35 1.543688 2.227018 1.502494 2.144084

6 0.40 1.740763 2.447863 1.678826 2.338775

7 0.45 1.941709 2.673463 1.822482 2.559144

8 0.50 2.148455 2.906051 2.153119 2.824701

9 0.55 2.363103 3.148210 2.156969 3.041831

10 0.60 2.588396 3.403113 2.495657 3.298120

11 0.65 2.827875 3.675011 2.653846 3.582761

12 0.70 3.086402 3.969703 2.847948 3.842405

13 0.75 3.371132 4.295856 3.076347 4.163895

14 0.80 3.693412 4.667286 3.523163 4.543075

15 0.85 4.073518 5.108783 3.869020 4.913774

16 0.90 4.554986 5.673582 4.372097 5.482038

DML CVaR Y(0) lower DML CVaR Y(0) upper DML CVaR Y(1) lower \

0 0.162710 0.558655 0.957745

1 0.360801 0.821021 1.175284

2 0.606342 1.052745 1.393604

3 0.824889 1.205187 1.601061

4 1.009428 1.397140 1.824750

5 1.292028 1.712960 2.041147

6 1.455078 1.902573 2.234534

7 1.579238 2.065725 2.455107

8 1.883914 2.422325 2.715407

9 1.907491 2.406446 2.932027

10 2.250210 2.741104 3.183526

11 2.382872 2.924821 3.466440

12 2.554076 3.141820 3.722848

13 2.727976 3.424717 4.041284

14 3.140833 3.905494 4.409746

15 3.483717 4.254324 4.773177

16 3.921372 4.822822 5.313209

DML CVaR Y(1) upper

0 1.158178

1 1.371429

2 1.585793

3 1.792939

4 2.026723

5 2.247020

6 2.443016

7 2.663182

8 2.933996

9 3.151636

10 3.412714

11 3.699082

12 3.961962

13 4.286507

14 4.676405

15 5.054370

16 5.650867

[7]:

from matplotlib import pyplot as plt

plt.rcParams['figure.figsize'] = 10., 7.5

fig, (ax1, ax2) = plt.subplots(1 ,2)

ax1.grid(); ax2.grid()

ax1.plot(df['Quantile'],df['DML CVaR Y(0)'], color='violet', label='Estimated CVaR Y(0)')

ax1.plot(df['Quantile'],df['CVaR Y(0)'], color='green', label='True CVaR Y(0)')

ax1.fill_between(df['Quantile'], df['DML CVaR Y(0) lower'], df['DML CVaR Y(0) upper'], color='violet', alpha=.3, label='Confidence Interval')

ax1.legend()

ax1.set_ylim(-2, 6)

ax2.plot(df['Quantile'],df['DML CVaR Y(1)'], color='violet', label='Estimated CVaR Y(1)')

ax2.plot(df['Quantile'],df['CVaR Y(1)'], color='green', label='True CVaR Y(1)')

ax2.fill_between(df['Quantile'], df['DML CVaR Y(1) lower'], df['DML CVaR Y(1) upper'], color='violet', alpha=.3, label='Confidence Interval')

ax2.legend()

ax2.set_ylim(-2, 6)

fig.suptitle('Conditional Value at Risk', fontsize=16)

fig.supxlabel('Quantile')

_ = fig.supylabel('CVaR and 95%-CI')

CVaR Treatment Effects#

In most cases, we want to evaluate the treatment effect on the CVaR as the difference between potential CVaRs. To estimate the treatment effect, we can use the DoubleMLQTE object and specify CVaR as the score.

As for quantile treatment effects, different quantiles can be estimated in parallel with n_jobs_models.

[8]:

n_cores = multiprocessing.cpu_count()

cores_used = np.min([5, n_cores - 1])

print(f"Number of Cores used: {cores_used}")

dml_CVAR = dml.DoubleMLQTE(obj_dml_data,

ml_g,

ml_m,

score='CVaR',

quantiles=tau_vec,

n_folds=5)

dml_CVAR.fit(n_jobs_models=cores_used)

print(dml_CVAR)

Number of Cores used: 5

================== DoubleMLQTE Object ==================

------------------ Fit summary ------------------

coef std err t P>|t| 2.5 % 97.5 %

0.10 0.627564 0.103806 6.045553 1.488982e-09 0.424108 0.831019

0.15 0.677980 0.102616 6.606954 3.923084e-11 0.476856 0.879103

0.20 0.706645 0.100356 7.041387 1.903366e-12 0.509951 0.903339

0.25 0.716793 0.102775 6.974414 3.071543e-12 0.515358 0.918227

0.30 0.716762 0.107073 6.694154 2.169220e-11 0.506903 0.926621

0.35 0.740869 0.112216 6.602168 4.051870e-11 0.520930 0.960808

0.40 0.756969 0.114647 6.602628 4.039302e-11 0.532266 0.981672

0.45 0.751710 0.117710 6.386102 1.701672e-10 0.521002 0.982417

0.50 0.779682 0.122408 6.369556 1.895768e-10 0.539767 1.019596

0.55 0.786744 0.130370 6.034690 1.592681e-09 0.531223 1.042265

0.60 0.814351 0.138378 5.884996 3.980643e-09 0.543136 1.085566

0.65 0.848868 0.144800 5.862359 4.563374e-09 0.565066 1.132671

0.70 0.946968 0.154828 6.116274 9.578847e-10 0.643512 1.250425

0.75 0.997621 0.164805 6.053331 1.418806e-09 0.674609 1.320633

0.80 1.073520 0.190915 5.623024 1.876431e-08 0.699333 1.447706

0.85 1.053558 0.236008 4.464076 8.041491e-06 0.590991 1.516125

0.90 1.097468 0.338908 3.238251 1.202650e-03 0.433221 1.761714

As for standard DoubleMLCVAR objects, we can construct valid confidencebands with the confint() method. Additionally, it might be helpful to construct uniformly valid confidence regions via boostrap.

[9]:

ci_CVAR = dml_CVAR.confint(level=0.95, joint=False)

dml_CVAR.bootstrap(n_rep_boot=2000)

ci_joint_CVAR = dml_CVAR.confint(level=0.95, joint=True)

print(ci_joint_CVAR)

2.5 % 97.5 %

0.10 0.367571 0.887556

0.15 0.420967 0.934992

0.20 0.455293 0.957996

0.25 0.459383 0.974202

0.30 0.448587 0.984937

0.35 0.459812 1.021926

0.40 0.469825 1.044113

0.45 0.456892 1.046527

0.50 0.473099 1.086264

0.55 0.460218 1.113270

0.60 0.467770 1.160932

0.65 0.486202 1.211534

0.70 0.559186 1.334750

0.75 0.584849 1.410393

0.80 0.595353 1.551686

0.85 0.462451 1.644665

0.90 0.248638 1.946297

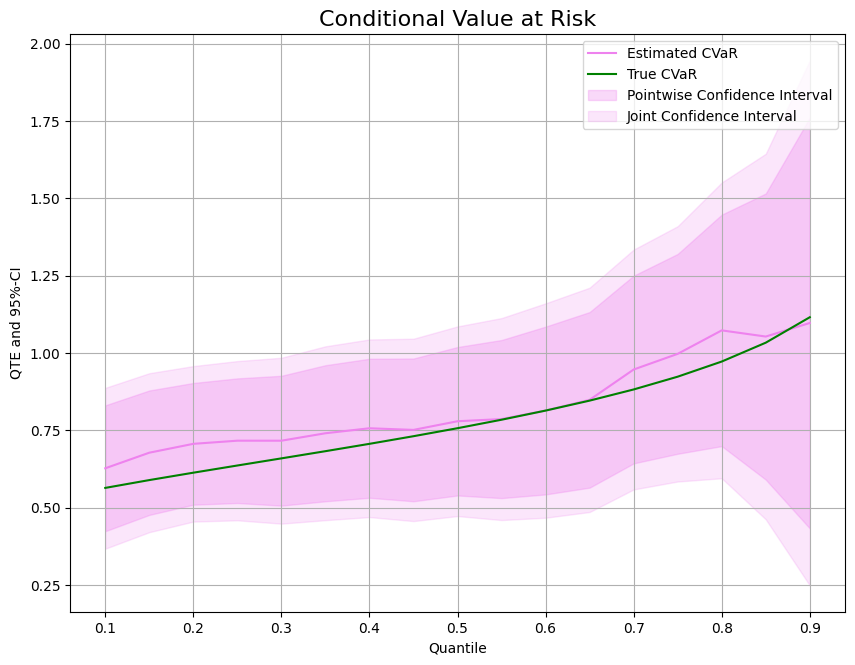

Finally, we can compare the predicted treatment effect with the true treatment effect on the CVaR.

[10]:

CVAR = np.array(Y1_cvar) - np.array(Y0_cvar)

data = {"Quantile": tau_vec, "CVaR": CVAR, "DML CVaR": dml_CVAR.coef,

"DML CVaR pointwise lower": ci_CVAR['2.5 %'], "DML CVaR pointwise upper": ci_CVAR['97.5 %'],

"DML CVaR joint lower": ci_joint_CVAR['2.5 %'], "DML CVaR joint upper": ci_joint_CVAR['97.5 %']}

df = pd.DataFrame(data)

print(df)

Quantile CVaR DML CVaR DML CVaR pointwise lower \

0.10 0.10 0.564829 0.627564 0.424108

0.15 0.15 0.590098 0.677980 0.476856

0.20 0.20 0.613950 0.706645 0.509951

0.25 0.25 0.637108 0.716793 0.515358

0.30 0.30 0.660128 0.716762 0.506903

0.35 0.35 0.683331 0.740869 0.520930

0.40 0.40 0.707101 0.756969 0.532266

0.45 0.45 0.731754 0.751710 0.521002

0.50 0.50 0.757596 0.779682 0.539767

0.55 0.55 0.785107 0.786744 0.531223

0.60 0.60 0.814717 0.814351 0.543136

0.65 0.65 0.847136 0.848868 0.565066

0.70 0.70 0.883301 0.946968 0.643512

0.75 0.75 0.924724 0.997621 0.674609

0.80 0.80 0.973874 1.073520 0.699333

0.85 0.85 1.035265 1.053558 0.590991

0.90 0.90 1.118596 1.097468 0.433221

DML CVaR pointwise upper DML CVaR joint lower DML CVaR joint upper

0.10 0.831019 0.367571 0.887556

0.15 0.879103 0.420967 0.934992

0.20 0.903339 0.455293 0.957996

0.25 0.918227 0.459383 0.974202

0.30 0.926621 0.448587 0.984937

0.35 0.960808 0.459812 1.021926

0.40 0.981672 0.469825 1.044113

0.45 0.982417 0.456892 1.046527

0.50 1.019596 0.473099 1.086264

0.55 1.042265 0.460218 1.113270

0.60 1.085566 0.467770 1.160932

0.65 1.132671 0.486202 1.211534

0.70 1.250425 0.559186 1.334750

0.75 1.320633 0.584849 1.410393

0.80 1.447706 0.595353 1.551686

0.85 1.516125 0.462451 1.644665

0.90 1.761714 0.248638 1.946297

[11]:

plt.rcParams['figure.figsize'] = 10., 7.5

fig, ax = plt.subplots()

ax.grid()

ax.plot(df['Quantile'],df['DML CVaR'], color='violet', label='Estimated CVaR')

ax.plot(df['Quantile'],df['CVaR'], color='green', label='True CVaR')

ax.fill_between(df['Quantile'], df['DML CVaR pointwise lower'], df['DML CVaR pointwise upper'], color='violet', alpha=.3, label='Pointwise Confidence Interval')

ax.fill_between(df['Quantile'], df['DML CVaR joint lower'], df['DML CVaR joint upper'], color='violet', alpha=.2, label='Joint Confidence Interval')

plt.legend()

plt.title('Conditional Value at Risk', fontsize=16)

plt.xlabel('Quantile')

_ = plt.ylabel('QTE and 95%-CI')