Note

-

Download Jupyter notebook:

https://docs.doubleml.org/stable/examples/py_double_ml_pension.ipynb.

Python: Impact of 401(k) on Financial Wealth#

In this real-data example, we illustrate how the DoubleML package can be used to estimate the effect of 401(k) eligibility and participation on accumulated assets. The 401(k) data set has been analyzed in several studies, among others Chernozhukov et al. (2018).

401(k) plans are pension accounts sponsored by employers. The key problem in determining the effect of participation in 401(k) plans on accumulated assets is saver heterogeneity coupled with the fact that the decision to enroll in a 401(k) is non-random. It is generally recognized that some people have a higher preference for saving than others. It also seems likely that those individuals with high unobserved preference for saving would be most likely to choose to participate in tax-advantaged retirement savings plans and would tend to have otherwise high amounts of accumulated assets. The presence of unobserved savings preferences with these properties then implies that conventional estimates that do not account for saver heterogeneity and endogeneity of participation will be biased upward, tending to overstate the savings effects of 401(k) participation.

One can argue that eligibility for enrolling in a 401(k) plan in this data can be taken as exogenous after conditioning on a few observables of which the most important for their argument is income. The basic idea is that, at least around the time 401(k)’s initially became available, people were unlikely to be basing their employment decisions on whether an employer offered a 401(k) but would instead focus on income and other aspects of the job.

Data#

The preprocessed data can be fetched by calling fetch_401K(). Note that an internet connection is required for loading the data.

[1]:

import numpy as np

import pandas as pd

import doubleml as dml

from doubleml.datasets import fetch_401K

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LassoCV, LogisticRegressionCV

from sklearn.ensemble import RandomForestClassifier, RandomForestRegressor

from sklearn.tree import DecisionTreeClassifier, DecisionTreeRegressor

from sklearn.preprocessing import StandardScaler

from sklearn.pipeline import make_pipeline

from xgboost import XGBClassifier, XGBRegressor

import matplotlib.pyplot as plt

import seaborn as sns

[2]:

sns.set()

colors = sns.color_palette()

[3]:

plt.rcParams['figure.figsize'] = 10., 7.5

sns.set(font_scale=1.5)

sns.set_style('whitegrid', {'axes.spines.top': False,

'axes.spines.bottom': False,

'axes.spines.left': False,

'axes.spines.right': False})

[4]:

data = fetch_401K(return_type='DataFrame')

[5]:

print(data.head())

nifa net_tfa tw age inc fsize educ db marr twoearn \

0 0.0 0.0 4500.0 47 6765.0 2 8 0 0 0

1 6215.0 1015.0 22390.0 36 28452.0 1 16 0 0 0

2 0.0 -2000.0 -2000.0 37 3300.0 6 12 1 0 0

3 15000.0 15000.0 155000.0 58 52590.0 2 16 0 1 1

4 0.0 0.0 58000.0 32 21804.0 1 11 0 0 0

e401 p401 pira hown

0 0 0 0 1

1 0 0 0 1

2 0 0 0 0

3 0 0 0 1

4 0 0 0 1

[6]:

print(data.describe())

nifa net_tfa tw age inc \

count 9.915000e+03 9.915000e+03 9.915000e+03 9915.000000 9915.000000

mean 1.392864e+04 1.805153e+04 6.381684e+04 41.060212 37200.621094

std 5.490488e+04 6.352250e+04 1.115297e+05 10.344505 24774.289062

min 0.000000e+00 -5.023020e+05 -5.023020e+05 25.000000 -2652.000000

25% 2.000000e+02 -5.000000e+02 3.291500e+03 32.000000 19413.000000

50% 1.635000e+03 1.499000e+03 2.510000e+04 40.000000 31476.000000

75% 8.765500e+03 1.652450e+04 8.148750e+04 48.000000 48583.500000

max 1.430298e+06 1.536798e+06 2.029910e+06 64.000000 242124.000000

fsize educ db marr twoearn \

count 9915.000000 9915.000000 9915.000000 9915.000000 9915.000000

mean 2.865860 13.206253 0.271004 0.604841 0.380837

std 1.538937 2.810382 0.444500 0.488909 0.485617

min 1.000000 1.000000 0.000000 0.000000 0.000000

25% 2.000000 12.000000 0.000000 0.000000 0.000000

50% 3.000000 12.000000 0.000000 1.000000 0.000000

75% 4.000000 16.000000 1.000000 1.000000 1.000000

max 13.000000 18.000000 1.000000 1.000000 1.000000

e401 p401 pira hown

count 9915.000000 9915.000000 9915.000000 9915.000000

mean 0.371357 0.261624 0.242158 0.635199

std 0.483192 0.439541 0.428411 0.481399

min 0.000000 0.000000 0.000000 0.000000

25% 0.000000 0.000000 0.000000 0.000000

50% 0.000000 0.000000 0.000000 1.000000

75% 1.000000 1.000000 0.000000 1.000000

max 1.000000 1.000000 1.000000 1.000000

The data consist of 9,915 observations at the household level drawn from the 1991 Survey of Income and Program Participation (SIPP). All the variables are referred to 1990. We use net financial assets (net_tfa) as the outcome variable, \(Y\), in our analysis. The net financial assets are computed as the sum of IRA balances, 401(k) balances, checking accounts, saving bonds, other interest-earning accounts, other interest-earning assets, stocks, and mutual funds less non mortgage debts.

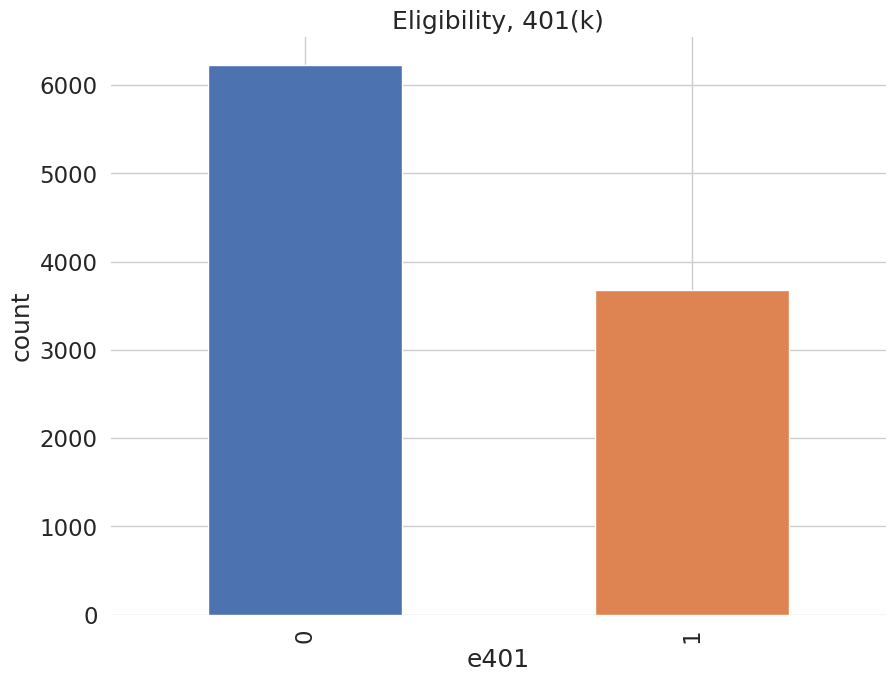

Among the \(9915\) individuals, \(3682\) are eligible to participate in the program. The variable e401 indicates eligibility and p401 indicates participation, respectively.

[7]:

data['e401'].value_counts().plot(kind='bar', color=colors)

plt.title('Eligibility, 401(k)')

plt.xlabel('e401')

_ = plt.ylabel('count')

[8]:

data['p401'].value_counts().plot(kind='bar', color=colors)

plt.title('Participation, 401(k)')

plt.xlabel('p401')

_ = plt.ylabel('count')

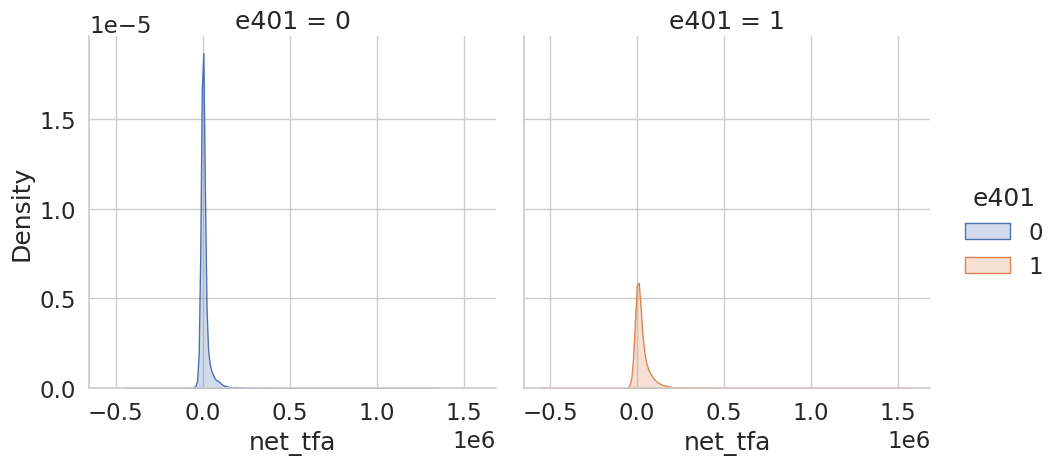

Eligibility is highly associated with financial wealth:

[9]:

_ = sns.displot(data, x="net_tfa", hue="e401", col="e401",

kind="kde", fill=True)

As a first estimate, we calculate the unconditional average predictive effect (APE) of 401(k) eligibility on accumulated assets. This effect corresponds to the average treatment effect if 401(k) eligibility would be assigned to individuals in an entirely randomized way. The unconditional APE of e401 is about \(19559\):

[10]:

print(data[['e401', 'net_tfa']].groupby('e401').mean().diff())

net_tfa

e401

0 NaN

1 19559.34375

Among the \(3682\) individuals that are eligible, \(2594\) decided to participate in the program. The unconditional APE of p401 is about \(27372\):

[11]:

print(data[['p401', 'net_tfa']].groupby('p401').mean().diff())

net_tfa

p401

0 NaN

1 27371.582031

As discussed, these estimates are biased since they do not account for saver heterogeneity and endogeneity of participation.

The DoubleML package#

Let’s use the package DoubleML to estimate the average treatment effect of 401(k) eligibility, i.e. e401, and participation, i.e. p401, on net financial assets net_tfa.

Estimating the Average Treatment Effect of 401(k) Eligibility on Net Financial Assets#

We first look at the treatment effect of e401 on net total financial assets. We give estimates of the ATE in the linear model

where \(f(X)\) is a dictonary applied to the raw regressors. \(X\) contains variables on marital status, two-earner status, defined benefit pension status, IRA participation, home ownership, family size, education, age, and income.

In the following, we will consider two different models,

a basic model specification that includes the raw regressors, i.e., \(f(X) = X\), and

a flexible model specification, where \(f(X)\) includes the raw regressors \(X\) and the orthogonal polynomials of degree 2 for the variables family size education, age, and income.

We will use the basic model specification whenever we use nonlinear methods, for example regression trees or random forests, and use the flexible model for linear methods such as the lasso. There are, of course, multiple ways how the model can be specified even more flexibly, for example including interactions of variable and higher order interaction. However, for the sake of simplicity we stick to the specification above. Users who are interested in varying the model can adapt the code below accordingly, for example to implement the orignal specification in Chernozhukov et al. (2018).

In the first step, we report estimates of the average treatment effect (ATE) of 401(k) eligibility on net financial assets both in the partially linear regression (PLR) model and in the interactive regression model (IRM) allowing for heterogeneous treatment effects.

The Data Backend: DoubleMLData#

To start our analysis, we initialize the data backend, i.e., a new instance of a DoubleMLData object. We implement the regression model by using scikit-learn’s PolynomialFeatures class.

To implement both models (basic and flexible), we generate two data backends: data_dml_base and data_dml_flex.

[12]:

# Set up basic model: Specify variables for data-backend

features_base = ['age', 'inc', 'educ', 'fsize', 'marr',

'twoearn', 'db', 'pira', 'hown']

# Initialize DoubleMLData (data-backend of DoubleML)

data_dml_base = dml.DoubleMLData(data,

y_col='net_tfa',

d_cols='e401',

x_cols=features_base)

[13]:

print(data_dml_base)

================== DoubleMLData Object ==================

------------------ Data summary ------------------

Outcome variable: net_tfa

Treatment variable(s): ['e401']

Covariates: ['age', 'inc', 'educ', 'fsize', 'marr', 'twoearn', 'db', 'pira', 'hown']

Instrument variable(s): None

No. Observations: 9915

------------------ DataFrame info ------------------

<class 'pandas.DataFrame'>

RangeIndex: 9915 entries, 0 to 9914

Columns: 14 entries, nifa to hown

dtypes: float32(4), int8(10)

memory usage: 251.9 KB

[14]:

# Set up a model according to regression formula with polynomials

features = data.copy()[['marr', 'twoearn', 'db', 'pira', 'hown']]

poly_dict = {'age': 2,

'inc': 2,

'educ': 2,

'fsize': 2}

for key, degree in poly_dict.items():

poly = PolynomialFeatures(degree, include_bias=False)

data_transf = poly.fit_transform(data[[key]])

x_cols = poly.get_feature_names_out([key])

data_transf = pd.DataFrame(data_transf, columns=x_cols)

features = pd.concat((features, data_transf),

axis=1, sort=False)

model_data = pd.concat((data.copy()[['net_tfa', 'e401']], features.copy()),

axis=1, sort=False)

# Initialize DoubleMLData (data-backend of DoubleML)

data_dml_flex = dml.DoubleMLData(model_data, y_col='net_tfa', d_cols='e401')

[15]:

print(data_dml_flex)

================== DoubleMLData Object ==================

------------------ Data summary ------------------

Outcome variable: net_tfa

Treatment variable(s): ['e401']

Covariates: ['marr', 'twoearn', 'db', 'pira', 'hown', 'age', 'age^2', 'inc', 'inc^2', 'educ', 'educ^2', 'fsize', 'fsize^2']

Instrument variable(s): None

No. Observations: 9915

------------------ DataFrame info ------------------

<class 'pandas.DataFrame'>

RangeIndex: 9915 entries, 0 to 9914

Columns: 15 entries, net_tfa to fsize^2

dtypes: float32(3), float64(6), int8(6)

memory usage: 639.2 KB

Partially Linear Regression Model (PLR)#

We start using lasso to estimate the function \(g_0\) and \(m_0\) in the following PLR model:

To estimate the causal parameter \(\theta_0\) here, we use double machine learning with 3-fold cross-fitting.

Estimation of the nuisance components \(g_0\) and \(m_0\), is based on the lasso with cross-validated choice of the penalty term , \(\lambda\), as provided by scikit-learn. We load the learner by initializing instances from the classes LassoCV and LogisticRegressionCV. Hyperparameters and options can be set during instantiation of the learner. Here we specify that the lasso should use that value of \(\lambda\) that minimizes the cross-validated mean squared error which is based on 5-fold cross validation.

We start by estimation the ATE in the basic model and then repeat the estimation in the flexible model.

[16]:

# Initialize learners

Cs = 0.0001*np.logspace(0, 4, 10)

lasso = make_pipeline(StandardScaler(), LassoCV(cv=5, max_iter=10000))

lasso_class = make_pipeline(StandardScaler(),

LogisticRegressionCV(cv=5, penalty='l1', solver='liblinear',

Cs = Cs, max_iter=1000))

np.random.seed(123)

# Initialize DoubleMLPLR model

dml_plr_lasso = dml.DoubleMLPLR(data_dml_base,

ml_l = lasso,

ml_m = lasso_class,

n_folds = 3)

dml_plr_lasso.fit(store_predictions=True)

print(dml_plr_lasso.summary)

coef std err t P>|t| 2.5 % 97.5 %

e401 5722.460744 1380.579125 4.144971 0.000034 3016.575381 8428.346107

[17]:

# Estimate the ATE in the flexible model with lasso

np.random.seed(123)

dml_plr_lasso = dml.DoubleMLPLR(data_dml_flex,

ml_l = lasso,

ml_m = lasso_class,

n_folds = 3)

dml_plr_lasso.fit(store_predictions=True)

lasso_summary = dml_plr_lasso.summary

print(lasso_summary)

coef std err t P>|t| 2.5 % \

e401 8974.791097 1324.323636 6.776887 1.227932e-11 6379.164467

97.5 %

e401 11570.417727

Alternatively, we can repeat this procedure with other machine learning methods, for example a random forest learner as provided by the RandomForestRegressor and RandomForestClassifier class in scikit-learn.

[18]:

# Random Forest

randomForest = RandomForestRegressor(

n_estimators=500, max_depth=7, max_features=3, min_samples_leaf=3)

randomForest_class = RandomForestClassifier(

n_estimators=500, max_depth=5, max_features=4, min_samples_leaf=7)

np.random.seed(123)

dml_plr_forest = dml.DoubleMLPLR(data_dml_base,

ml_l = randomForest,

ml_m = randomForest_class,

n_folds = 3)

dml_plr_forest.fit(store_predictions=True)

forest_summary = dml_plr_forest.summary

print(forest_summary)

coef std err t P>|t| 2.5 % \

e401 8909.634078 1321.822289 6.740417 1.579322e-11 6318.909997

97.5 %

e401 11500.358158

Now, let’s use a regression tree as provided in scikit-learn’s DecisionTreeRegressor and DecisionTreeClassifier.

[19]:

# Trees

trees = DecisionTreeRegressor(

max_depth=30, ccp_alpha=0.0047, min_samples_split=203, min_samples_leaf=67)

trees_class = DecisionTreeClassifier(

max_depth=30, ccp_alpha=0.0042, min_samples_split=104, min_samples_leaf=34)

np.random.seed(123)

dml_plr_tree = dml.DoubleMLPLR(data_dml_base,

ml_l = trees,

ml_m = trees_class,

n_folds = 3)

dml_plr_tree.fit(store_predictions=True)

tree_summary = dml_plr_tree.summary

print(tree_summary)

coef std err t P>|t| 2.5 % \

e401 8260.06428 1348.624798 6.124805 9.079458e-10 5616.808246

97.5 %

e401 10903.320314

We can also experiment with extreme gradient boosting as provided by xgboost.

[20]:

# Boosted Trees

boost = XGBRegressor(n_jobs=1, objective = "reg:squarederror",

eta=0.1, n_estimators=35)

boost_class = XGBClassifier(use_label_encoder=False, n_jobs=1,

objective = "binary:logistic", eval_metric = "logloss",

eta=0.1, n_estimators=34)

np.random.seed(123)

dml_plr_boost = dml.DoubleMLPLR(data_dml_base,

ml_l = boost,

ml_m = boost_class,

n_folds = 3)

dml_plr_boost.fit(store_predictions=True)

boost_summary = dml_plr_boost.summary

print(boost_summary)

coef std err t P>|t| 2.5 % \

e401 8336.661463 1391.026647 5.993172 2.057874e-09 5610.299334

97.5 %

e401 11063.023593

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/xgboost/training.py:200: UserWarning: [11:46:47] WARNING: /__w/xgboost/xgboost/src/learner.cc:794:

Parameters: { "use_label_encoder" } are not used.

bst.update(dtrain, iteration=i, fobj=obj)

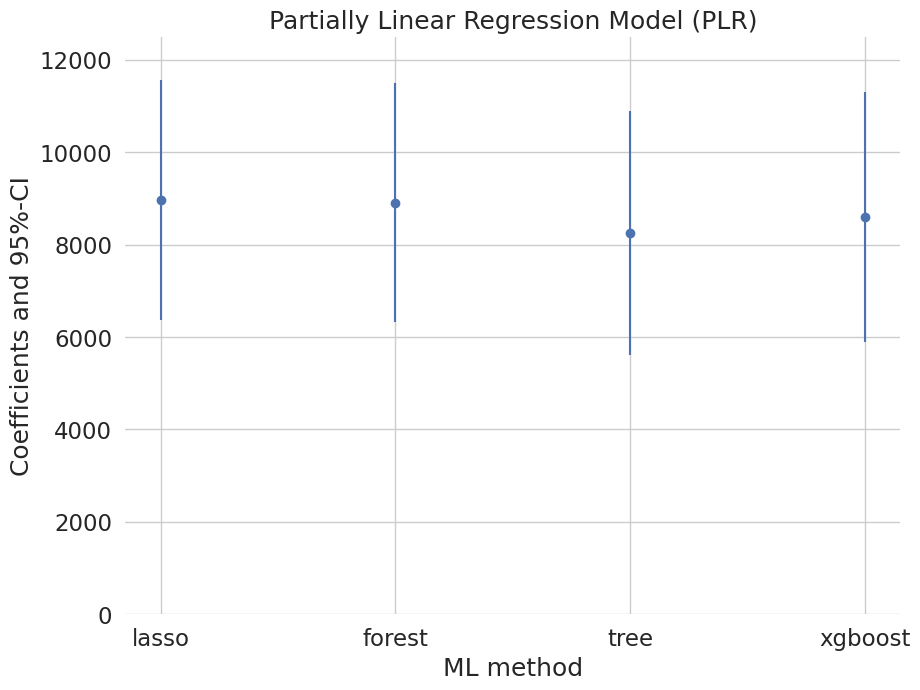

Let’s sum up the results:

[21]:

plr_summary = pd.concat((lasso_summary, forest_summary, tree_summary, boost_summary))

plr_summary.index = ['lasso', 'forest', 'tree', 'xgboost']

print(plr_summary[['coef', '2.5 %', '97.5 %']])

coef 2.5 % 97.5 %

lasso 8974.791097 6379.164467 11570.417727

forest 8909.634078 6318.909997 11500.358158

tree 8260.064280 5616.808246 10903.320314

xgboost 8336.661463 5610.299334 11063.023593

[22]:

errors = np.full((2, plr_summary.shape[0]), np.nan)

errors[0, :] = plr_summary['coef'] - plr_summary['2.5 %']

errors[1, :] = plr_summary['97.5 %'] - plr_summary['coef']

plt.errorbar(plr_summary.index, plr_summary.coef, fmt='o', yerr=errors)

plt.ylim([0, 12500])

plt.title('Partially Linear Regression Model (PLR)')

plt.xlabel('ML method')

_ = plt.ylabel('Coefficients and 95%-CI')

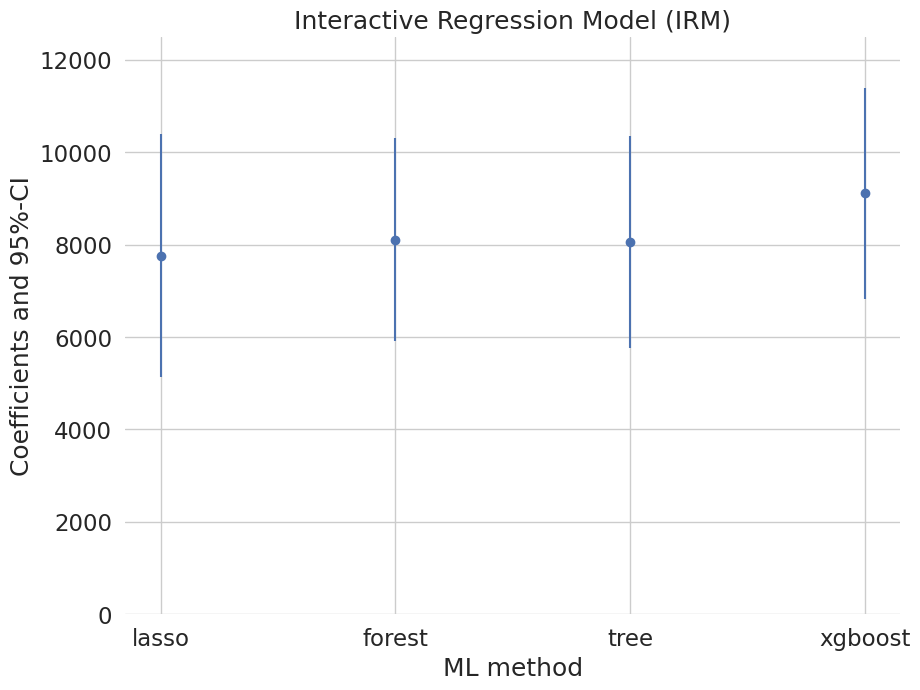

Interactive Regression Model (IRM)#

Next, we consider estimation of average treatment effects when treatment effects are fully heterogeneous:

To reduce the disproportionate impact of extreme propensity score weights in the interactive model we trim the propensity scores which are close to the bounds.

[23]:

# Lasso

lasso = make_pipeline(StandardScaler(), LassoCV(cv=5, max_iter=20000))

# Initialize DoubleMLIRM model

np.random.seed(123)

dml_irm_lasso = dml.DoubleMLIRM(data_dml_flex,

ml_g = lasso,

ml_m = lasso_class,

trimming_threshold = 0.01,

n_folds = 3)

dml_irm_lasso.fit(store_predictions=True)

lasso_summary = dml_irm_lasso.summary

print(lasso_summary)

coef std err t P>|t| 2.5 % \

e401 7763.891606 1343.034846 5.780856 7.432130e-09 5131.591678

97.5 %

e401 10396.191534

[24]:

# Random Forest

randomForest = RandomForestRegressor(n_estimators=500)

randomForest_class = RandomForestClassifier(n_estimators=500)

np.random.seed(123)

dml_irm_forest = dml.DoubleMLIRM(data_dml_base,

ml_g = randomForest,

ml_m = randomForest_class,

trimming_threshold = 0.01,

n_folds = 3)

# Set nuisance-part specific parameters

dml_irm_forest.set_ml_nuisance_params('ml_g0', 'e401', {

'max_depth': 6, 'max_features': 4, 'min_samples_leaf': 7})

dml_irm_forest.set_ml_nuisance_params('ml_g1', 'e401', {

'max_depth': 6, 'max_features': 3, 'min_samples_leaf': 5})

dml_irm_forest.set_ml_nuisance_params('ml_m', 'e401', {

'max_depth': 6, 'max_features': 3, 'min_samples_leaf': 6})

dml_irm_forest.fit(store_predictions=True)

forest_summary = dml_irm_forest.summary

print(forest_summary)

coef std err t P>|t| 2.5 % \

e401 8102.443032 1120.75171 7.229472 4.848757e-13 5905.810044

97.5 %

e401 10299.076019

[25]:

# Trees

trees = DecisionTreeRegressor(max_depth=30)

trees_class = DecisionTreeClassifier(max_depth=30)

np.random.seed(123)

dml_irm_tree = dml.DoubleMLIRM(data_dml_base,

ml_g = trees,

ml_m = trees_class,

trimming_threshold = 0.01,

n_folds = 3)

# Set nuisance-part specific parameters

dml_irm_tree.set_ml_nuisance_params('ml_g0', 'e401', {

'ccp_alpha': 0.0016, 'min_samples_split': 74, 'min_samples_leaf': 24})

dml_irm_tree.set_ml_nuisance_params('ml_g1', 'e401', {

'ccp_alpha': 0.0018, 'min_samples_split': 70, 'min_samples_leaf': 23})

dml_irm_tree.set_ml_nuisance_params('ml_m', 'e401', {

'ccp_alpha': 0.0028, 'min_samples_split': 167, 'min_samples_leaf': 55})

dml_irm_tree.fit(store_predictions=True)

tree_summary = dml_irm_tree.summary

print(tree_summary)

coef std err t P>|t| 2.5 % \

e401 8059.691511 1167.841132 6.90136 5.150719e-12 5770.764953

97.5 %

e401 10348.618069

[26]:

# Boosted Trees

boost = XGBRegressor(n_jobs=1, objective = "reg:squarederror")

boost_class = XGBClassifier(use_label_encoder=False, n_jobs=1,

objective = "binary:logistic", eval_metric = "logloss")

np.random.seed(123)

dml_irm_boost = dml.DoubleMLIRM(data_dml_base,

ml_g = boost,

ml_m = boost_class,

trimming_threshold = 0.01,

n_folds = 3)

# Set nuisance-part specific parameters

dml_irm_boost.set_ml_nuisance_params('ml_g0', 'e401', {

'eta': 0.1, 'n_estimators': 8})

dml_irm_boost.set_ml_nuisance_params('ml_g1', 'e401', {

'eta': 0.1, 'n_estimators': 29})

dml_irm_boost.set_ml_nuisance_params('ml_m', 'e401', {

'eta': 0.1, 'n_estimators': 23})

dml_irm_boost.fit(store_predictions=True)

boost_summary = dml_irm_boost.summary

print(boost_summary)

coef std err t P>|t| 2.5 % \

e401 8989.440854 1191.377446 7.545418 4.508390e-14 6654.383968

97.5 %

e401 11324.497739

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/xgboost/training.py:200: UserWarning: [11:47:04] WARNING: /__w/xgboost/xgboost/src/learner.cc:794:

Parameters: { "use_label_encoder" } are not used.

bst.update(dtrain, iteration=i, fobj=obj)

[27]:

irm_summary = pd.concat((lasso_summary, forest_summary, tree_summary, boost_summary))

irm_summary.index = ['lasso', 'forest', 'tree', 'xgboost']

print(irm_summary[['coef', '2.5 %', '97.5 %']])

coef 2.5 % 97.5 %

lasso 7763.891606 5131.591678 10396.191534

forest 8102.443032 5905.810044 10299.076019

tree 8059.691511 5770.764953 10348.618069

xgboost 8989.440854 6654.383968 11324.497739

[28]:

errors = np.full((2, irm_summary.shape[0]), np.nan)

errors[0, :] = irm_summary['coef'] - irm_summary['2.5 %']

errors[1, :] = irm_summary['97.5 %'] - irm_summary['coef']

plt.errorbar(irm_summary.index, irm_summary.coef, fmt='o', yerr=errors)

plt.ylim([0, 12500])

plt.title('Interactive Regression Model (IRM)')

plt.xlabel('ML method')

_ = plt.ylabel('Coefficients and 95%-CI')

These estimates that flexibly account for confounding are substantially attenuated relative to the baseline estimate (19559) that does not account for confounding. They suggest much smaller causal effects of 401(k) eligiblity on financial asset holdings.

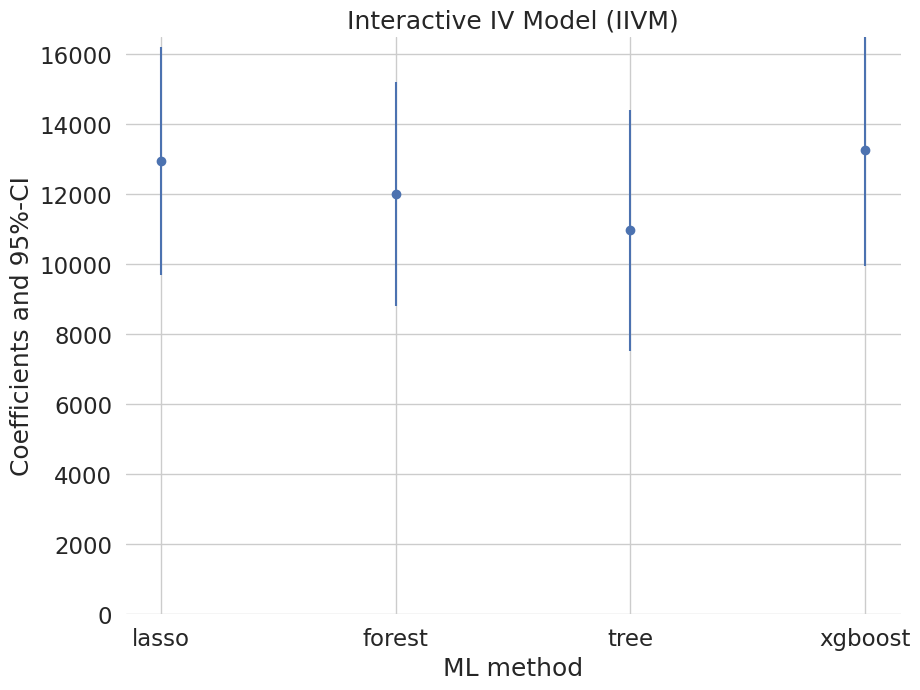

Local Average Treatment Effects of 401(k) Participation on Net Financial Assets#

Interactive IV Model (IIVM)#

In the examples above, we estimated the average treatment effect of eligibility on financial asset holdings. Now, we consider estimation of local average treatment effects (LATE) of participation using eligibility as an instrument for the participation decision. Under appropriate assumptions, the LATE identifies the treatment effect for so-called compliers, i.e., individuals who would only participate if eligible and otherwise not participate in the program.

As before, \(Y\) denotes the outcome net_tfa, and \(X\) is the vector of covariates. We use e401 as a binary instrument for the treatment variable p401. Here the structural equation model is:

[29]:

# Initialize DoubleMLData with an instrument

# Basic model

data_dml_base_iv = dml.DoubleMLData(data,

y_col='net_tfa',

d_cols='p401',

z_cols='e401',

x_cols=features_base)

print(data_dml_base_iv)

================== DoubleMLData Object ==================

------------------ Data summary ------------------

Outcome variable: net_tfa

Treatment variable(s): ['p401']

Covariates: ['age', 'inc', 'educ', 'fsize', 'marr', 'twoearn', 'db', 'pira', 'hown']

Instrument variable(s): ['e401']

No. Observations: 9915

------------------ DataFrame info ------------------

<class 'pandas.DataFrame'>

RangeIndex: 9915 entries, 0 to 9914

Columns: 14 entries, nifa to hown

dtypes: float32(4), int8(10)

memory usage: 251.9 KB

[30]:

# Flexible model

model_data = pd.concat((data.copy()[['net_tfa', 'e401', 'p401']], features.copy()),

axis=1, sort=False)

data_dml_iv_flex = dml.DoubleMLData(model_data,

y_col='net_tfa',

d_cols='p401',

z_cols='e401')

print(data_dml_iv_flex)

================== DoubleMLData Object ==================

------------------ Data summary ------------------

Outcome variable: net_tfa

Treatment variable(s): ['p401']

Covariates: ['marr', 'twoearn', 'db', 'pira', 'hown', 'age', 'age^2', 'inc', 'inc^2', 'educ', 'educ^2', 'fsize', 'fsize^2']

Instrument variable(s): ['e401']

No. Observations: 9915

------------------ DataFrame info ------------------

<class 'pandas.DataFrame'>

RangeIndex: 9915 entries, 0 to 9914

Columns: 16 entries, net_tfa to fsize^2

dtypes: float32(3), float64(6), int8(7)

memory usage: 648.9 KB

[31]:

# Lasso

lasso = make_pipeline(StandardScaler(), LassoCV(cv=5, max_iter=20000))

# Initialize DoubleMLIRM model

np.random.seed(123)

dml_iivm_lasso = dml.DoubleMLIIVM(data_dml_iv_flex,

ml_g = lasso,

ml_m = lasso_class,

ml_r = lasso_class,

subgroups = {'always_takers': False,

'never_takers': True},

trimming_threshold = 0.01,

n_folds = 3)

dml_iivm_lasso.fit(store_predictions=True)

lasso_summary = dml_iivm_lasso.summary

print(lasso_summary)

coef std err t P>|t| 2.5 % \

p401 12955.591652 1661.333581 7.798308 6.274251e-15 9699.437667

97.5 %

p401 16211.745638

Again, we repeat the procedure for the other machine learning methods:

[32]:

# Random Forest

randomForest = RandomForestRegressor(n_estimators=500)

randomForest_class = RandomForestClassifier(n_estimators=500)

np.random.seed(123)

dml_iivm_forest = dml.DoubleMLIIVM(data_dml_base_iv,

ml_g = randomForest,

ml_m = randomForest_class,

ml_r = randomForest_class,

subgroups = {'always_takers': False,

'never_takers': True},

trimming_threshold = 0.01,

n_folds = 3)

# Set nuisance-part specific parameters

dml_iivm_forest.set_ml_nuisance_params('ml_g0', 'p401', {

'max_depth': 6, 'max_features': 4, 'min_samples_leaf': 7})

dml_iivm_forest.set_ml_nuisance_params('ml_g1', 'p401', {

'max_depth': 6, 'max_features': 3, 'min_samples_leaf': 5})

dml_iivm_forest.set_ml_nuisance_params('ml_m', 'p401', {

'max_depth': 6, 'max_features': 3, 'min_samples_leaf': 6})

dml_iivm_forest.set_ml_nuisance_params('ml_r1', 'p401', {

'max_depth': 4, 'max_features': 7, 'min_samples_leaf': 6})

dml_iivm_forest.fit(store_predictions=True)

forest_summary = dml_iivm_forest.summary

print(forest_summary)

coef std err t P>|t| 2.5 % \

p401 12002.712592 1628.619613 7.369869 1.707963e-13 8810.676807

97.5 %

p401 15194.748377

[33]:

# Trees

trees = DecisionTreeRegressor(max_depth=30)

trees_class = DecisionTreeClassifier(max_depth=30)

np.random.seed(123)

dml_iivm_tree = dml.DoubleMLIIVM(data_dml_base_iv,

ml_g = trees,

ml_m = trees_class,

ml_r = trees_class,

subgroups = {'always_takers': False,

'never_takers': True},

trimming_threshold = 0.01,

n_folds = 3)

# Set nuisance-part specific parameters

dml_iivm_tree.set_ml_nuisance_params('ml_g0', 'p401', {

'ccp_alpha': 0.0016, 'min_samples_split': 74, 'min_samples_leaf': 24})

dml_iivm_tree.set_ml_nuisance_params('ml_g1', 'p401', {

'ccp_alpha': 0.0018, 'min_samples_split': 70, 'min_samples_leaf': 23})

dml_iivm_tree.set_ml_nuisance_params('ml_m', 'p401', {

'ccp_alpha': 0.0028, 'min_samples_split': 167, 'min_samples_leaf': 55})

dml_iivm_tree.set_ml_nuisance_params('ml_r1', 'p401', {

'ccp_alpha': 0.0576, 'min_samples_split': 55, 'min_samples_leaf': 18})

dml_iivm_tree.fit(store_predictions=True)

tree_summary = dml_iivm_tree.summary

print(tree_summary)

coef std err t P>|t| 2.5 % \

p401 10967.290987 1751.863772 6.260356 3.840995e-10 7533.701088

97.5 %

p401 14400.880886

[34]:

# Boosted Trees

boost = XGBRegressor(n_jobs=1, objective = "reg:squarederror")

boost_class = XGBClassifier(use_label_encoder=False, n_jobs=1,

objective = "binary:logistic", eval_metric = "logloss")

np.random.seed(123)

dml_iivm_boost = dml.DoubleMLIIVM(data_dml_base_iv,

ml_g = boost,

ml_m = boost_class,

ml_r = boost_class,

subgroups = {'always_takers': False,

'never_takers': True},

trimming_threshold = 0.01,

n_folds = 3)

# Set nuisance-part specific parameters

dml_iivm_boost.set_ml_nuisance_params('ml_g0', 'p401', {

'eta': 0.1, 'n_estimators': 9})

dml_iivm_boost.set_ml_nuisance_params('ml_g1', 'p401', {

'eta': 0.1, 'n_estimators': 33})

dml_iivm_boost.set_ml_nuisance_params('ml_m', 'p401', {

'eta': 0.1, 'n_estimators': 12})

dml_iivm_boost.set_ml_nuisance_params('ml_r1', 'p401', {

'eta': 0.1, 'n_estimators': 25})

dml_iivm_boost.fit(store_predictions=True)

boost_summary = dml_iivm_boost.summary

print(boost_summary)

coef std err t P>|t| 2.5 % \

p401 13312.769647 1672.359011 7.960474 1.713821e-15 10035.006217

97.5 %

p401 16590.533077

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/xgboost/training.py:200: UserWarning: [11:47:25] WARNING: /__w/xgboost/xgboost/src/learner.cc:794:

Parameters: { "use_label_encoder" } are not used.

bst.update(dtrain, iteration=i, fobj=obj)

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/xgboost/training.py:200: UserWarning: [11:47:25] WARNING: /__w/xgboost/xgboost/src/learner.cc:794:

Parameters: { "use_label_encoder" } are not used.

bst.update(dtrain, iteration=i, fobj=obj)

[35]:

iivm_summary = pd.concat((lasso_summary, forest_summary, tree_summary, boost_summary))

iivm_summary.index = ['lasso', 'forest', 'tree', 'xgboost']

print(iivm_summary[['coef', '2.5 %', '97.5 %']])

coef 2.5 % 97.5 %

lasso 12955.591652 9699.437667 16211.745638

forest 12002.712592 8810.676807 15194.748377

tree 10967.290987 7533.701088 14400.880886

xgboost 13312.769647 10035.006217 16590.533077

[36]:

colors = sns.color_palette()

[37]:

errors = np.full((2, iivm_summary.shape[0]), np.nan)

errors[0, :] = iivm_summary['coef'] - iivm_summary['2.5 %']

errors[1, :] = iivm_summary['97.5 %'] - iivm_summary['coef']

plt.errorbar(iivm_summary.index, iivm_summary.coef, fmt='o', yerr=errors)

plt.ylim([0, 16500])

plt.title('Interactive IV Model (IIVM)')

plt.xlabel('ML method')

_ = plt.ylabel('Coefficients and 95%-CI')

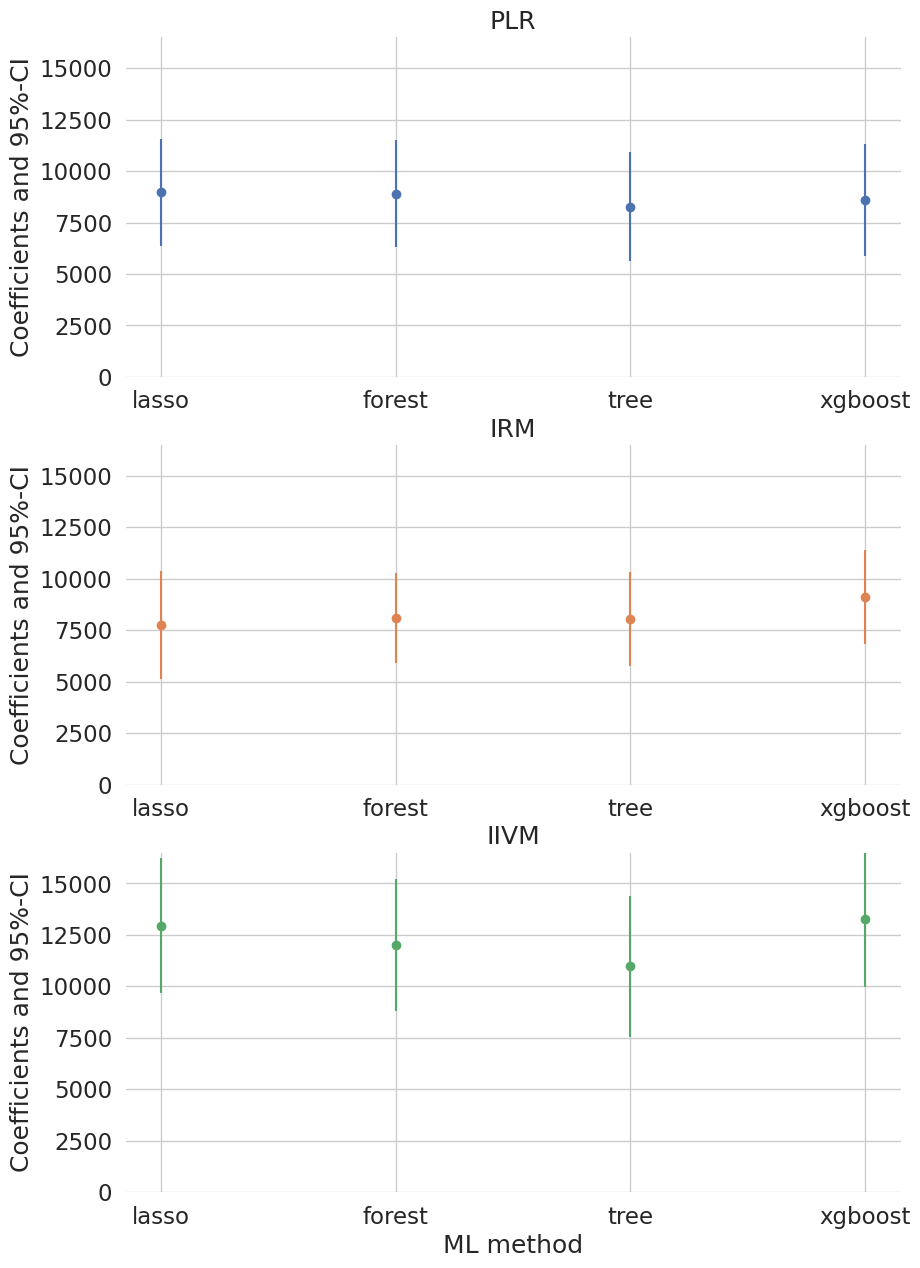

Summary of Results#

To sum up, let’s merge all our results so far and illustrate them in a plot.

[38]:

df_summary = pd.concat((plr_summary, irm_summary, iivm_summary)).reset_index().rename(columns={'index': 'ML'})

df_summary['Model'] = np.concatenate((np.repeat('PLR', 4), np.repeat('IRM', 4), np.repeat('IIVM', 4)))

print(df_summary.set_index(['Model', 'ML']))

coef std err t P>|t| \

Model ML

PLR lasso 8974.791097 1324.323636 6.776887 1.227932e-11

forest 8909.634078 1321.822289 6.740417 1.579322e-11

tree 8260.064280 1348.624798 6.124805 9.079458e-10

xgboost 8336.661463 1391.026647 5.993172 2.057874e-09

IRM lasso 7763.891606 1343.034846 5.780856 7.432130e-09

forest 8102.443032 1120.751710 7.229472 4.848757e-13

tree 8059.691511 1167.841132 6.901360 5.150719e-12

xgboost 8989.440854 1191.377446 7.545418 4.508390e-14

IIVM lasso 12955.591652 1661.333581 7.798308 6.274251e-15

forest 12002.712592 1628.619613 7.369869 1.707963e-13

tree 10967.290987 1751.863772 6.260356 3.840995e-10

xgboost 13312.769647 1672.359011 7.960474 1.713821e-15

2.5 % 97.5 %

Model ML

PLR lasso 6379.164467 11570.417727

forest 6318.909997 11500.358158

tree 5616.808246 10903.320314

xgboost 5610.299334 11063.023593

IRM lasso 5131.591678 10396.191534

forest 5905.810044 10299.076019

tree 5770.764953 10348.618069

xgboost 6654.383968 11324.497739

IIVM lasso 9699.437667 16211.745638

forest 8810.676807 15194.748377

tree 7533.701088 14400.880886

xgboost 10035.006217 16590.533077

[39]:

plt.figure(figsize=(10, 15))

colors = sns.color_palette()

for ind, model in enumerate(['PLR', 'IRM', 'IIVM']):

plt.subplot(3, 1, ind+1)

this_df = df_summary.query('Model == @model')

errors = np.full((2, this_df.shape[0]), np.nan)

errors[0, :] = this_df['coef'] - this_df['2.5 %']

errors[1, :] = this_df['97.5 %'] - this_df['coef']

plt.errorbar(this_df.ML, this_df.coef, fmt='o', yerr=errors,

color=colors[ind], ecolor=colors[ind])

plt.ylim([0, 16500])

plt.title(model)

plt.ylabel('Coefficients and 95%-CI')

_ = plt.xlabel('ML method')

We report results based on four ML methods for estimating the nuisance functions used in forming the orthogonal estimating equations. We find again that the estimates of the treatment effect are stable across ML methods. The estimates are highly significant, hence we would reject the hypothesis that 401(k) participation has no effect on financial wealth.

Acknowledgement

We would like to thank Jannis Kueck for sharing the kaggle notebook. The pension data set has been analyzed in several studies, among others Chernozhukov et al. (2018).