Note

-

Download Jupyter notebook:

https://docs.doubleml.org/stable/examples/did/py_panel.ipynb.

Python: Panel Data with Multiple Time Periods#

In this example, a detailed guide on Difference-in-Differences with multiple time periods using the DoubleML-package. The implementation is based on Callaway and Sant’Anna(2021).

The notebook requires the following packages:

[1]:

import seaborn as sns

import matplotlib.pyplot as plt

import pandas as pd

import numpy as np

from lightgbm import LGBMRegressor, LGBMClassifier

from sklearn.linear_model import LinearRegression, LogisticRegression

from doubleml.did import DoubleMLDIDMulti

from doubleml.data import DoubleMLPanelData

from doubleml.did.datasets import make_did_CS2021

Data#

We will rely on the make_did_CS2021 DGP, which is inspired by Callaway and Sant’Anna(2021) (Appendix SC) and Sant’Anna and Zhao (2020).

We will observe n_obs units over n_periods. Remark that the dataframe includes observations of the potential outcomes y0 and y1, such that we can use oracle estimates as comparisons.

[2]:

n_obs = 5000

n_periods = 6

df = make_did_CS2021(n_obs, dgp_type=4, n_periods=n_periods, n_pre_treat_periods=3, time_type="datetime")

df["ite"] = df["y1"] - df["y0"]

print(df.shape)

df.head()

(30000, 11)

[2]:

| id | y | y0 | y1 | d | t | Z1 | Z2 | Z3 | Z4 | ite | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 203.750614 | 203.750614 | 202.740645 | 2025-04-01 | 2025-01-01 | -0.462824 | 0.940043 | 0.294488 | -0.482148 | -1.009969 |

| 1 | 0 | 197.523968 | 197.523968 | 199.167086 | 2025-04-01 | 2025-02-01 | -0.462824 | 0.940043 | 0.294488 | -0.482148 | 1.643118 |

| 2 | 0 | 194.910341 | 194.910341 | 194.635074 | 2025-04-01 | 2025-03-01 | -0.462824 | 0.940043 | 0.294488 | -0.482148 | -0.275267 |

| 3 | 0 | 190.400515 | 188.406164 | 190.400515 | 2025-04-01 | 2025-04-01 | -0.462824 | 0.940043 | 0.294488 | -0.482148 | 1.994351 |

| 4 | 0 | 186.277273 | 185.801651 | 186.277273 | 2025-04-01 | 2025-05-01 | -0.462824 | 0.940043 | 0.294488 | -0.482148 | 0.475621 |

Data Details#

Here, we slightly abuse the definition of the potential outcomes. \(Y_{i,t}(1)\) corresponds to the (potential) outcome if unit \(i\) would have received treatment at time period \(\mathrm{g}\) (where the group \(\mathrm{g}\) is drawn with probabilities based on \(Z\)).

More specifically

where

\(f_t(Z)\) depends on pre-treatment observable covariates \(Z_1,\dots, Z_4\) and time \(t\)

\(\delta_t\) is a time fixed effect

\(\eta_i\) is a unit fixed effect

\(\epsilon_{i,t,\cdot}\) are time varying unobservables (iid. \(N(0,1)\))

\(\theta_{i,t,\mathrm{g}}\) correponds to the exposure effect of unit \(i\) based on group \(\mathrm{g}\) at time \(t\)

For the pre-treatment periods the exposure effect is set to

such that

The DoubleML Coverage Repository includes coverage simulations based on this DGP.

Data Description#

The data is a balanced panel where each unit is observed over n_periods starting Janary 2025.

[3]:

df.groupby("t").size()

[3]:

t

2025-01-01 5000

2025-02-01 5000

2025-03-01 5000

2025-04-01 5000

2025-05-01 5000

2025-06-01 5000

dtype: int64

The treatment column d indicates first treatment period of the corresponding unit, whereas NaT units are never treated.

Generally, never treated units should take either on the value ``np.inf`` or ``pd.NaT`` depending on the data type (``float`` or ``datetime``).

The individual units are roughly uniformly divided between the groups, where treatment assignment depends on the pre-treatment covariates Z1 to Z4.

[4]:

df.groupby("d", dropna=False).size()

[4]:

d

2025-04-01 7962

2025-05-01 7164

2025-06-01 7074

NaT 7800

dtype: int64

Here, the group indicates the first treated period and NaT units are never treated. To simplify plotting and pands

[5]:

df.groupby("d", dropna=False).size()

[5]:

d

2025-04-01 7962

2025-05-01 7164

2025-06-01 7074

NaT 7800

dtype: int64

To get a better understanding of the underlying data and true effects, we will compare the unconditional averages and the true effects based on the oracle values of individual effects ite.

[6]:

# rename for plotting

df["First Treated"] = df["d"].dt.strftime("%Y-%m").fillna("Never Treated")

# Create aggregation dictionary for means

def agg_dict(col_name):

return {

f'{col_name}_mean': (col_name, 'mean'),

f'{col_name}_lower_quantile': (col_name, lambda x: x.quantile(0.05)),

f'{col_name}_upper_quantile': (col_name, lambda x: x.quantile(0.95))

}

# Calculate means and confidence intervals

agg_dictionary = agg_dict("y") | agg_dict("ite")

agg_df = df.groupby(["t", "First Treated"]).agg(**agg_dictionary).reset_index()

agg_df.head()

[6]:

| t | First Treated | y_mean | y_lower_quantile | y_upper_quantile | ite_mean | ite_lower_quantile | ite_upper_quantile | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2025-01-01 | 2025-04 | 208.966152 | 199.224528 | 219.250256 | 0.069582 | -2.215653 | 2.429346 |

| 1 | 2025-01-01 | 2025-05 | 210.646033 | 200.096640 | 221.249996 | 0.016820 | -2.322898 | 2.344836 |

| 2 | 2025-01-01 | 2025-06 | 212.414793 | 202.102566 | 222.432046 | 0.007513 | -2.366163 | 2.361266 |

| 3 | 2025-01-01 | Never Treated | 214.293697 | 204.060509 | 224.113516 | 0.034644 | -2.287565 | 2.370999 |

| 4 | 2025-02-01 | 2025-04 | 208.996551 | 189.581265 | 229.292453 | 0.029423 | -2.256231 | 2.514630 |

[7]:

def plot_data(df, col_name='y'):

"""

Create an improved plot with colorblind-friendly features

Parameters:

-----------

df : DataFrame

The dataframe containing the data

col_name : str, default='y'

Column name to plot (will use '{col_name}_mean')

"""

plt.figure(figsize=(12, 7))

n_colors = df["First Treated"].nunique()

color_palette = sns.color_palette("colorblind", n_colors=n_colors)

sns.lineplot(

data=df,

x='t',

y=f'{col_name}_mean',

hue='First Treated',

style='First Treated',

palette=color_palette,

markers=True,

dashes=True,

linewidth=2.5,

alpha=0.8

)

plt.title(f'Average Values {col_name} by Group Over Time', fontsize=16)

plt.xlabel('Time', fontsize=14)

plt.ylabel(f'Average Value {col_name}', fontsize=14)

plt.legend(title='First Treated', title_fontsize=13, fontsize=12,

frameon=True, framealpha=0.9, loc='best')

plt.grid(alpha=0.3, linestyle='-')

plt.tight_layout()

plt.show()

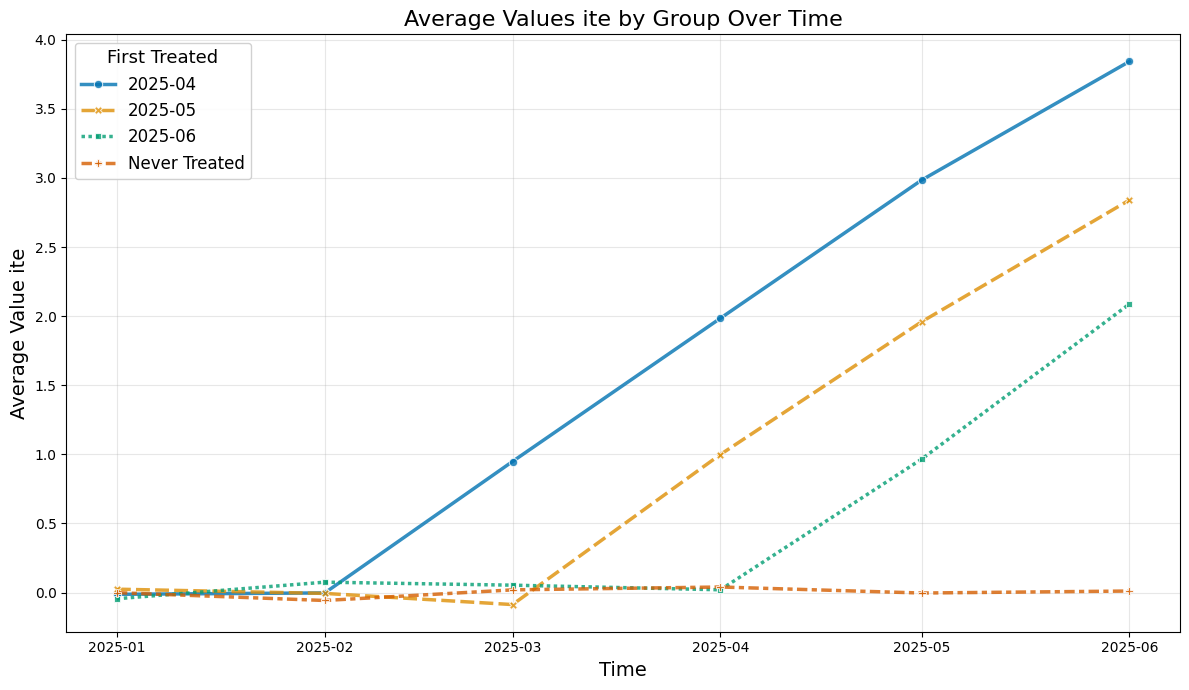

So let us take a look at the average values over time

[8]:

plot_data(agg_df, col_name='y')

Instead the true average treatment treatment effects can be obtained by averaging (usually unobserved) the ite values.

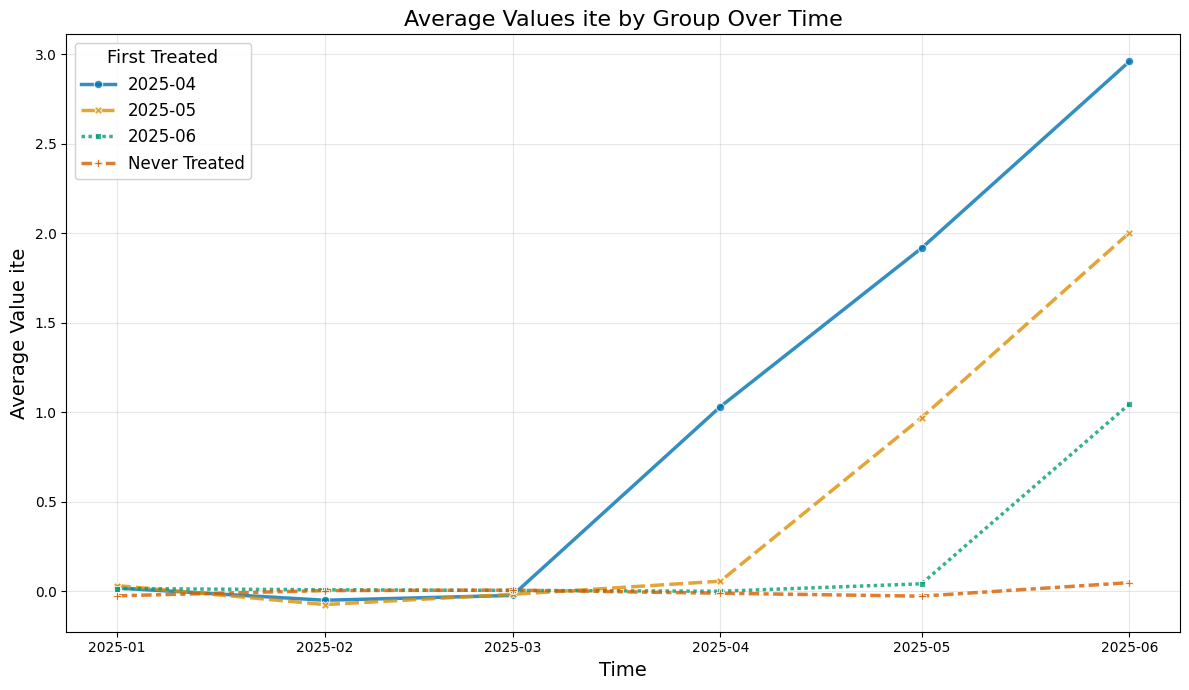

The true effect just equals the exposure time (in months):

[9]:

plot_data(agg_df, col_name='ite')

DoubleMLPanelData#

Finally, we can construct our DoubleMLPanelData, specifying

y_col: the outcomed_cols: the group variable indicating the first treated period for each unitid_col: the unique identification column for each unitt_col: the time columnx_cols: the additional pre-treatment controlsdatetime_unit: unit required fordatetimecolumns and plotting

[10]:

dml_data = DoubleMLPanelData(

data=df,

y_col="y",

d_cols="d",

id_col="id",

t_col="t",

x_cols=["Z1", "Z2", "Z3", "Z4"],

datetime_unit="M"

)

print(dml_data)

================== DoubleMLPanelData Object ==================

------------------ Data summary ------------------

Outcome variable: y

Treatment variable(s): ['d']

Covariates: ['Z1', 'Z2', 'Z3', 'Z4']

Instrument variable(s): None

Time variable: t

Id variable: id

Static panel data: False

No. Unique Ids: 5000

No. Observations: 30000

------------------ DataFrame info ------------------

<class 'pandas.DataFrame'>

RangeIndex: 30000 entries, 0 to 29999

Columns: 12 entries, id to First Treated

dtypes: datetime64[s](2), float64(8), int64(1), str(1)

memory usage: 2.7 MB

ATT Estimation#

The DoubleML-package implements estimation of group-time average treatment effect via the DoubleMLDIDMulti class (see model documentation).

Basics#

The class basically behaves like other DoubleML classes and requires the specification of two learners (for more details on the regression elements, see score documentation).

The basic arguments of a DoubleMLDIDMulti object include

ml_g“outcome” regression learnerml_mpropensity Score learnercontrol_groupthe control group for the parallel trend assumptiongt_combinationscombinations of \((\mathrm{g},t_\text{pre}, t_\text{eval})\)anticipation_periodsnumber of anticipation periods

We will construct a dict with “default” arguments.

[11]:

default_args = {

"ml_g": LGBMRegressor(n_estimators=500, learning_rate=0.01, verbose=-1, random_state=123),

"ml_m": LGBMClassifier(n_estimators=500, learning_rate=0.01, verbose=-1, random_state=123),

"control_group": "never_treated",

"gt_combinations": "standard",

"anticipation_periods": 0,

"n_folds": 5,

"n_rep": 1,

}

The model will be estimated using the fit() method.

[12]:

np.random.seed(42)

dml_obj = DoubleMLDIDMulti(dml_data, **default_args)

dml_obj.fit()

print(dml_obj)

================== DoubleMLDIDMulti Object ==================

------------------ Data summary ------------------

Outcome variable: y

Treatment variable(s): ['d']

Covariates: ['Z1', 'Z2', 'Z3', 'Z4']

Instrument variable(s): None

Time variable: t

Id variable: id

Static panel data: False

No. Unique Ids: 5000

No. Observations: 30000

------------------ Score & algorithm ------------------

Score function: observational

Control group: never_treated

Anticipation periods: 0

------------------ Machine learner ------------------

Learner ml_g: LGBMRegressor(learning_rate=0.01, n_estimators=500, random_state=123,

verbose=-1)

Learner ml_m: LGBMClassifier(learning_rate=0.01, n_estimators=500, random_state=123,

verbose=-1)

Out-of-sample Performance:

Regression:

Learner ml_g0 RMSE: [[1.91338358 1.88236051 1.99264942 2.87893822 3.8009951 1.90634126

1.84867211 1.98091665 1.87937269 2.77928034 1.90482482 1.86590244

1.96159196 1.87304141 1.92379882]]

Learner ml_g1 RMSE: [[1.84094653 1.97333765 1.88702737 2.64263606 3.70194641 1.86441151

1.89748067 1.92304046 1.90301857 2.76312121 1.9932098 1.97960121

1.96959464 2.00805025 2.00279502]]

Classification:

Learner ml_m Log Loss: [[0.68884788 0.69438633 0.68969147 0.68973574 0.68929964 0.72372452

0.7167171 0.71867106 0.72550416 0.71474318 0.72879418 0.72513805

0.7258349 0.72367139 0.72173017]]

------------------ Resampling ------------------

No. folds: 5

No. repeated sample splits: 1

------------------ Fit summary ------------------

coef std err t P>|t| \

ATT(2025-04,2025-01,2025-02) 0.049358 0.105945 0.465878 6.413027e-01

ATT(2025-04,2025-02,2025-03) 0.010778 0.103573 0.104065 9.171177e-01

ATT(2025-04,2025-03,2025-04) 0.987431 0.139868 7.059754 1.667999e-12

ATT(2025-04,2025-03,2025-05) 1.712670 0.197909 8.653837 0.000000e+00

ATT(2025-04,2025-03,2025-06) 2.774843 0.248031 11.187469 0.000000e+00

ATT(2025-05,2025-01,2025-02) -0.025096 0.097103 -0.258446 7.960630e-01

ATT(2025-05,2025-02,2025-03) -0.204573 0.098410 -2.078778 3.763776e-02

ATT(2025-05,2025-03,2025-04) -0.123023 0.096069 -1.280574 2.003435e-01

ATT(2025-05,2025-04,2025-05) 1.026166 0.097913 10.480358 0.000000e+00

ATT(2025-05,2025-04,2025-06) 1.730357 0.149501 11.574195 0.000000e+00

ATT(2025-06,2025-01,2025-02) 0.109712 0.094031 1.166760 2.433073e-01

ATT(2025-06,2025-02,2025-03) 0.000143 0.097444 0.001465 9.988311e-01

ATT(2025-06,2025-03,2025-04) -0.089618 0.097672 -0.917542 3.588588e-01

ATT(2025-06,2025-04,2025-05) -0.008012 0.100675 -0.079584 9.365684e-01

ATT(2025-06,2025-05,2025-06) 0.935033 0.101425 9.218968 0.000000e+00

2.5 % 97.5 %

ATT(2025-04,2025-01,2025-02) -0.158291 0.257006

ATT(2025-04,2025-02,2025-03) -0.192222 0.213778

ATT(2025-04,2025-03,2025-04) 0.713296 1.261567

ATT(2025-04,2025-03,2025-05) 1.324776 2.100565

ATT(2025-04,2025-03,2025-06) 2.288710 3.260975

ATT(2025-05,2025-01,2025-02) -0.215414 0.165222

ATT(2025-05,2025-02,2025-03) -0.397454 -0.011693

ATT(2025-05,2025-03,2025-04) -0.311314 0.065268

ATT(2025-05,2025-04,2025-05) 0.834260 1.218073

ATT(2025-05,2025-04,2025-06) 1.437340 2.023374

ATT(2025-06,2025-01,2025-02) -0.074586 0.294010

ATT(2025-06,2025-02,2025-03) -0.190843 0.191129

ATT(2025-06,2025-03,2025-04) -0.281051 0.101815

ATT(2025-06,2025-04,2025-05) -0.205332 0.189308

ATT(2025-06,2025-05,2025-06) 0.736244 1.133822

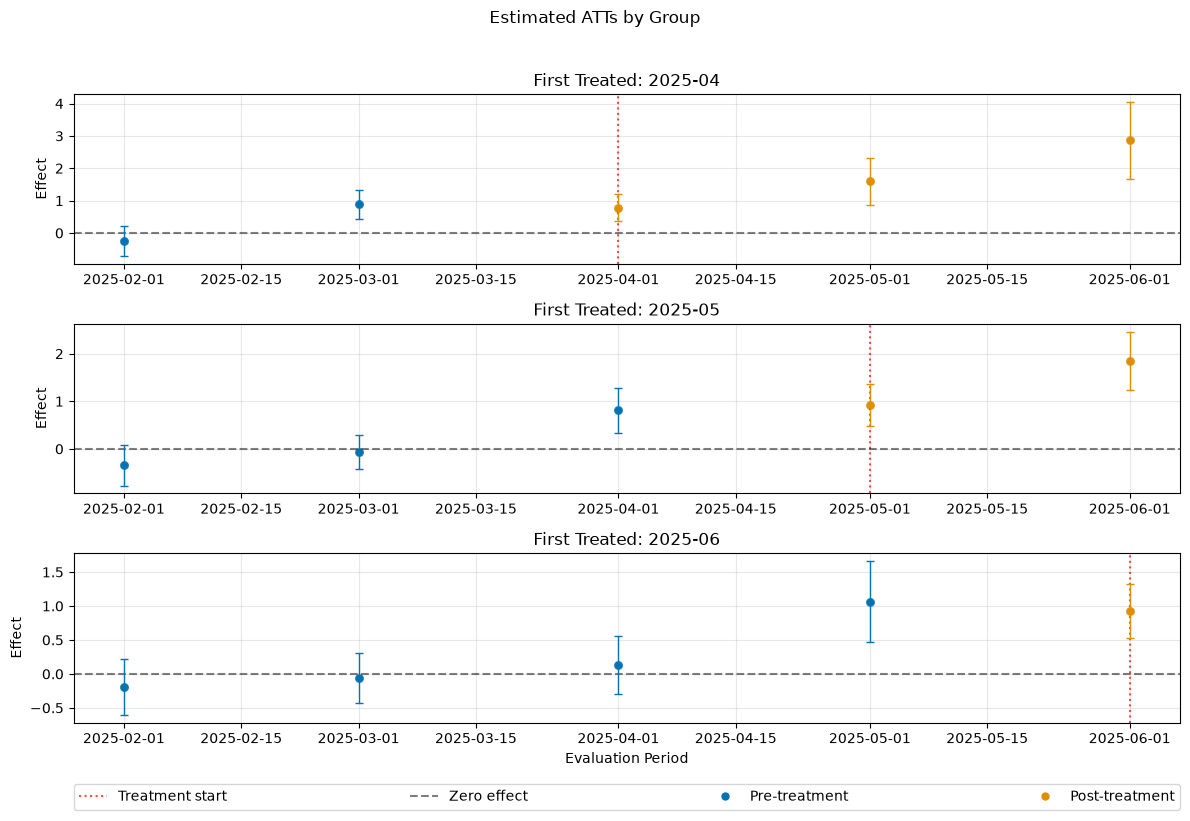

The summary displays estimates of the \(ATT(g,t_\text{eval})\) effects for different combinations of \((g,t_\text{eval})\) via \(\widehat{ATT}(\mathrm{g},t_\text{pre},t_\text{eval})\), where

\(\mathrm{g}\) specifies the group

\(t_\text{pre}\) specifies the corresponding pre-treatment period

\(t_\text{eval}\) specifies the evaluation period

The choice gt_combinations="standard", used estimates all possible combinations of \(ATT(g,t_\text{eval})\) via \(\widehat{ATT}(\mathrm{g},t_\text{pre},t_\text{eval})\), where the standard choice is \(t_\text{pre} = \min(\mathrm{g}, t_\text{eval}) - 1\) (without anticipation).

Remark that this includes pre-tests effects if \(\mathrm{g} > t_{eval}\), e.g. \(\widehat{ATT}(g=\text{2025-04}, t_{\text{pre}}=\text{2025-01}, t_{\text{eval}}=\text{2025-02})\) which estimates the pre-trend from January to February even if the actual treatment occured in April.

As usual for the DoubleML-package, you can obtain joint confidence intervals via bootstrap.

[13]:

level = 0.95

ci = dml_obj.confint(level=level)

dml_obj.bootstrap(n_rep_boot=5000)

ci_joint = dml_obj.confint(level=level, joint=True)

ci_joint

[13]:

| 2.5 % | 97.5 % | |

|---|---|---|

| ATT(2025-04,2025-01,2025-02) | -0.251866 | 0.350581 |

| ATT(2025-04,2025-02,2025-03) | -0.283702 | 0.305258 |

| ATT(2025-04,2025-03,2025-04) | 0.589759 | 1.385103 |

| ATT(2025-04,2025-03,2025-05) | 1.149976 | 2.275365 |

| ATT(2025-04,2025-03,2025-06) | 2.069640 | 3.480046 |

| ATT(2025-05,2025-01,2025-02) | -0.301179 | 0.250987 |

| ATT(2025-05,2025-02,2025-03) | -0.484374 | 0.075227 |

| ATT(2025-05,2025-03,2025-04) | -0.396166 | 0.150120 |

| ATT(2025-05,2025-04,2025-05) | 0.747779 | 1.304554 |

| ATT(2025-05,2025-04,2025-06) | 1.305295 | 2.155419 |

| ATT(2025-06,2025-01,2025-02) | -0.157638 | 0.377062 |

| ATT(2025-06,2025-02,2025-03) | -0.276909 | 0.277194 |

| ATT(2025-06,2025-03,2025-04) | -0.367319 | 0.188083 |

| ATT(2025-06,2025-04,2025-05) | -0.294252 | 0.278228 |

| ATT(2025-06,2025-05,2025-06) | 0.646661 | 1.223404 |

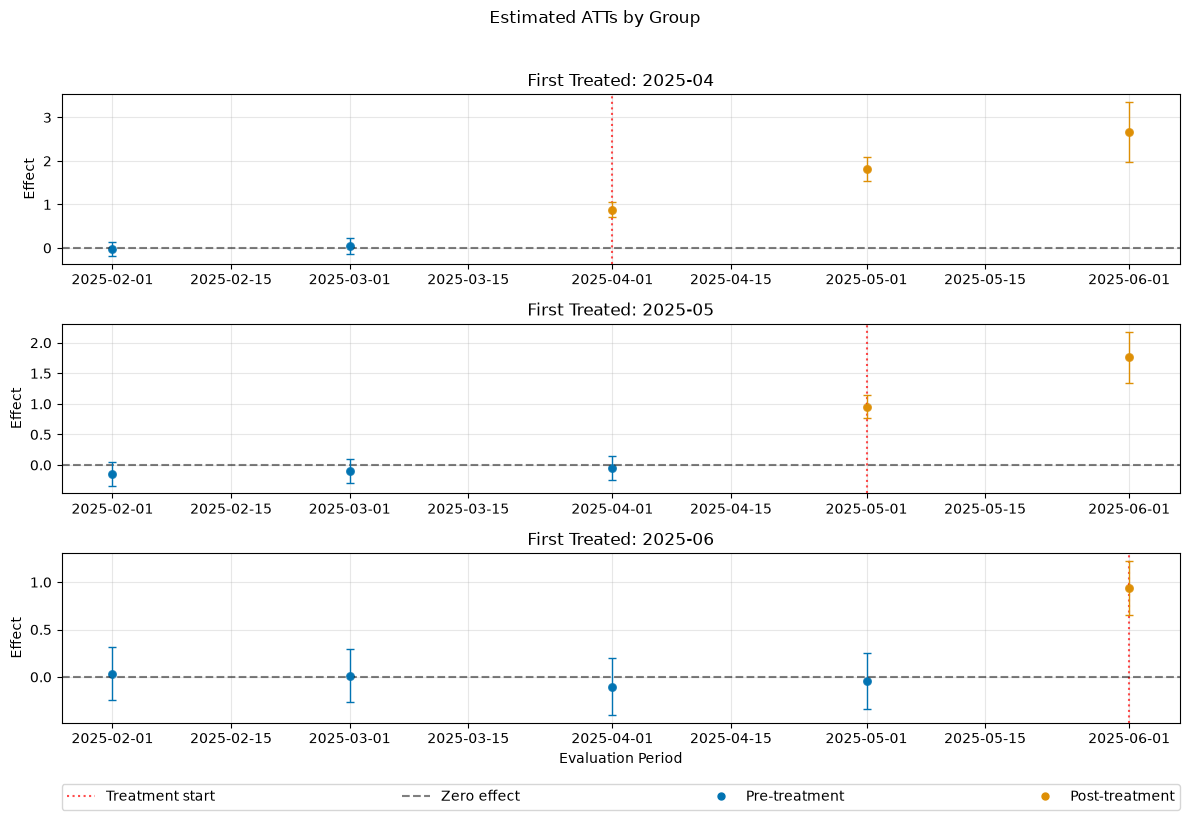

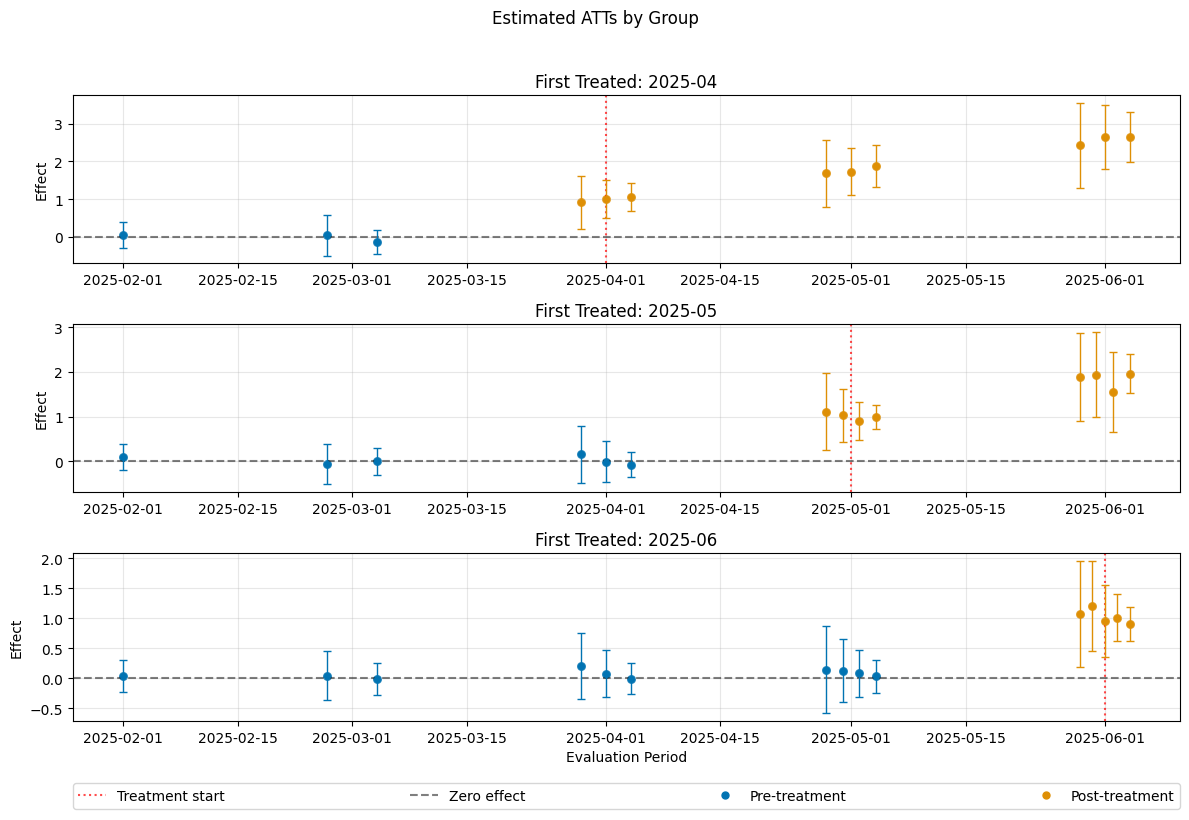

A visualization of the effects can be obtained via the plot_effects() method.

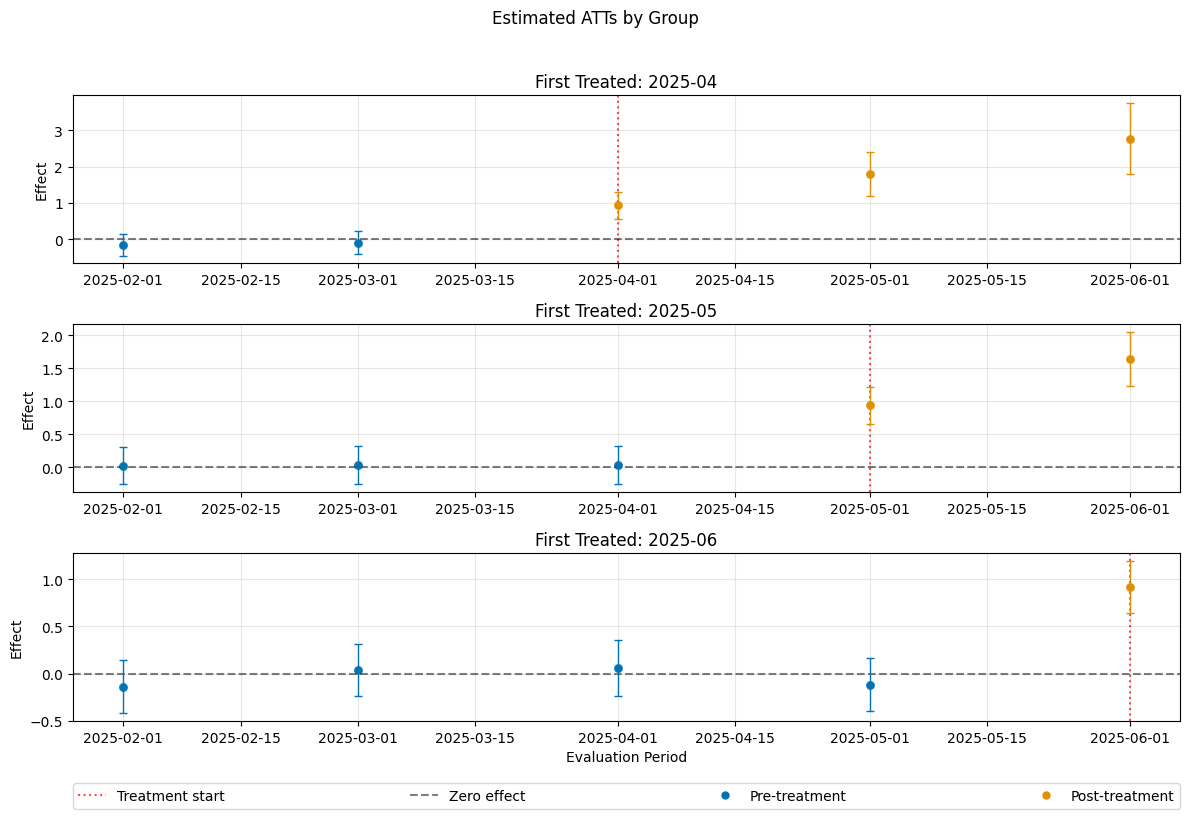

Remark that the plot used joint confidence intervals per default.

[14]:

dml_obj.plot_effects()

[14]:

(<Figure size 1200x800 with 4 Axes>,

[<Axes: title={'center': 'First Treated: 2025-04'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-05'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-06'}, xlabel='Evaluation Period', ylabel='Effect'>])

Sensitivity Analysis#

As descripted in the Sensitivity Guide, robustness checks on omitted confounding/parallel trend violations are available, via the standard sensitivity_analysis() method.

[15]:

dml_obj.sensitivity_analysis()

print(dml_obj.sensitivity_summary)

================== Sensitivity Analysis ==================

------------------ Scenario ------------------

Significance Level: level=0.95

Sensitivity parameters: cf_y=0.03; cf_d=0.03, rho=1.0

------------------ Bounds with CI ------------------

CI lower theta lower theta theta upper \

ATT(2025-04,2025-01,2025-02) -0.227648 -0.055618 0.049358 0.154333

ATT(2025-04,2025-02,2025-03) -0.258103 -0.088584 0.010778 0.110141

ATT(2025-04,2025-03,2025-04) 0.659822 0.881911 0.987431 1.092952

ATT(2025-04,2025-03,2025-05) 1.248944 1.568317 1.712670 1.857024

ATT(2025-04,2025-03,2025-06) 2.159335 2.559134 2.774843 2.990551

ATT(2025-05,2025-01,2025-02) -0.275788 -0.116707 -0.025096 0.066515

ATT(2025-05,2025-02,2025-03) -0.464630 -0.305402 -0.204573 -0.103745

ATT(2025-05,2025-03,2025-04) -0.384726 -0.227879 -0.123023 -0.018167

ATT(2025-05,2025-04,2025-05) 0.766926 0.925213 1.026166 1.127120

ATT(2025-05,2025-04,2025-06) 1.325383 1.569479 1.730357 1.891235

ATT(2025-06,2025-01,2025-02) -0.150403 0.003145 0.109712 0.216280

ATT(2025-06,2025-02,2025-03) -0.265853 -0.104821 0.000143 0.105107

ATT(2025-06,2025-03,2025-04) -0.356857 -0.198155 -0.089618 0.018918

ATT(2025-06,2025-04,2025-05) -0.278494 -0.114802 -0.008012 0.098778

ATT(2025-06,2025-05,2025-06) 0.660728 0.826966 0.935033 1.043100

CI upper

ATT(2025-04,2025-01,2025-02) 0.331802

ATT(2025-04,2025-02,2025-03) 0.283129

ATT(2025-04,2025-03,2025-04) 1.331689

ATT(2025-04,2025-03,2025-05) 2.190231

ATT(2025-04,2025-03,2025-06) 3.408017

ATT(2025-05,2025-01,2025-02) 0.228084

ATT(2025-05,2025-02,2025-03) 0.061470

ATT(2025-05,2025-03,2025-04) 0.141760

ATT(2025-05,2025-04,2025-05) 1.291540

ATT(2025-05,2025-04,2025-06) 2.139543

ATT(2025-06,2025-01,2025-02) 0.372621

ATT(2025-06,2025-02,2025-03) 0.265159

ATT(2025-06,2025-03,2025-04) 0.182262

ATT(2025-06,2025-04,2025-05) 0.266754

ATT(2025-06,2025-05,2025-06) 1.211150

------------------ Robustness Values ------------------

H_0 RV (%) RVa (%)

ATT(2025-04,2025-01,2025-02) 0.0 1.422091 0.000462

ATT(2025-04,2025-02,2025-03) 0.0 0.329718 0.000383

ATT(2025-04,2025-03,2025-04) 0.0 24.729599 20.460193

ATT(2025-04,2025-03,2025-05) 0.0 30.194391 25.149295

ATT(2025-04,2025-03,2025-06) 0.0 32.251724 28.362684

ATT(2025-05,2025-01,2025-02) 0.0 0.831100 0.000656

ATT(2025-05,2025-02,2025-03) 0.0 5.992154 1.243256

ATT(2025-05,2025-03,2025-04) 0.0 3.510552 0.000511

ATT(2025-05,2025-04,2025-05) 0.0 26.537853 22.964342

ATT(2025-05,2025-04,2025-06) 0.0 27.832232 24.344828

ATT(2025-06,2025-01,2025-02) 0.0 3.087203 0.000429

ATT(2025-06,2025-02,2025-03) 0.0 0.004004 0.000530

ATT(2025-06,2025-03,2025-04) 0.0 2.483751 0.000483

ATT(2025-06,2025-04,2025-05) 0.0 0.228122 0.000515

ATT(2025-06,2025-05,2025-06) 0.0 23.110356 19.230241

In this example one can clearly, distinguish the robustness of the non-zero effects vs. the pre-treatment periods.

Control Groups#

The current implementation support the following control groups

"never_treated""not_yet_treated"

Remark that the ``”not_yet_treated” depends on anticipation.

For differences and recommendations, we refer to Callaway and Sant’Anna(2021).

[16]:

dml_obj_nyt = DoubleMLDIDMulti(dml_data, **(default_args | {"control_group": "not_yet_treated"}))

dml_obj_nyt.fit()

dml_obj_nyt.bootstrap(n_rep_boot=5000)

dml_obj_nyt.plot_effects()

[16]:

(<Figure size 1200x800 with 4 Axes>,

[<Axes: title={'center': 'First Treated: 2025-04'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-05'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-06'}, xlabel='Evaluation Period', ylabel='Effect'>])

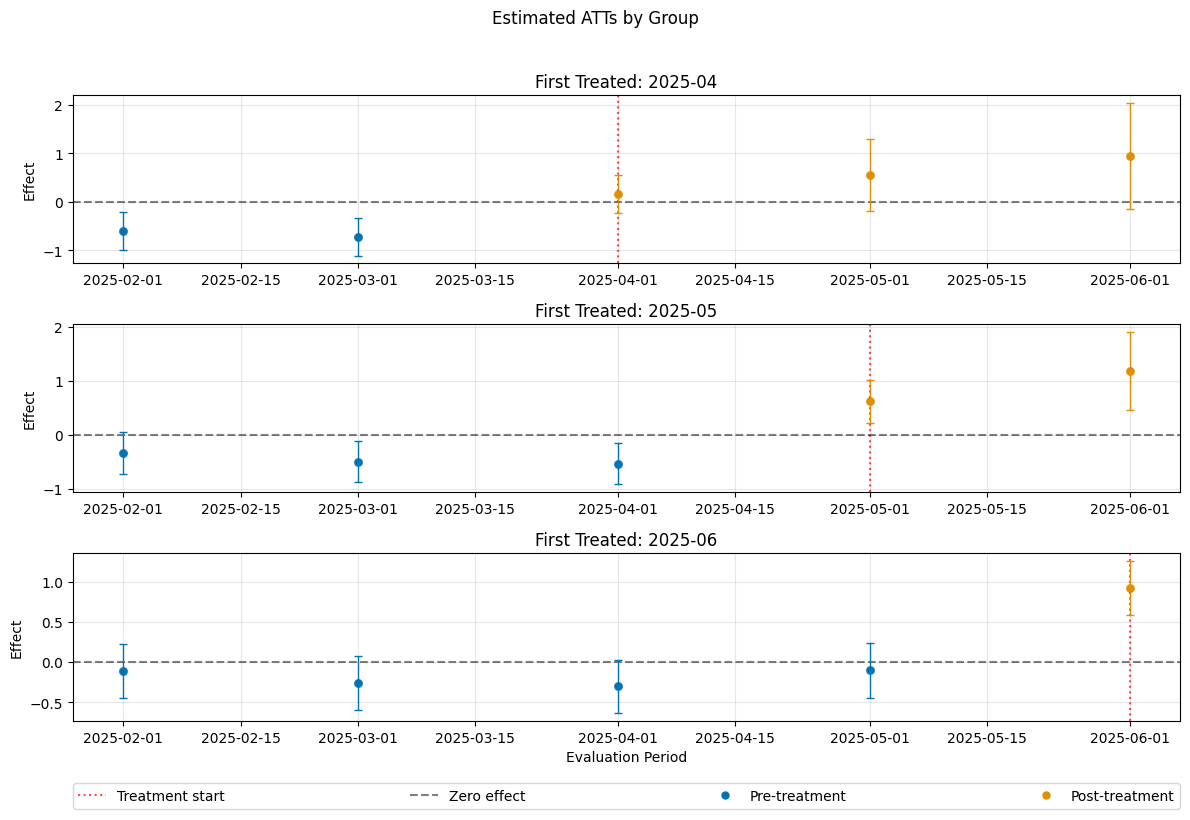

Linear Covariate Adjustment#

Remark that we relied on boosted trees to adjust for conditional parallel trends which allow for a nonlinear adjustment. In comparison to linear adjustment, we could rely on linear learners.

Remark that the DGP (``dgp_type=4``) is based on nonlinear conditional expectations such that the estimates will be biased

[17]:

linear_learners = {

"ml_g": LinearRegression(),

"ml_m": LogisticRegression(),

}

dml_obj_linear = DoubleMLDIDMulti(dml_data, **(default_args | linear_learners))

dml_obj_linear.fit()

dml_obj_linear.bootstrap(n_rep_boot=5000)

dml_obj_linear.plot_effects()

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

[17]:

(<Figure size 1200x800 with 4 Axes>,

[<Axes: title={'center': 'First Treated: 2025-04'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-05'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-06'}, xlabel='Evaluation Period', ylabel='Effect'>])

Aggregated Effects#

As the did-R-package, the \(ATT\)’s can be aggregated to summarize multiple effects. For details on different aggregations and details on their interpretations see Callaway and Sant’Anna(2021).

The aggregations are implemented via the aggregate() method.

Group Aggregation#

To obtain group-specific effects one can would like to average \(ATT(\mathrm{g}, t_\text{eval})\) over \(t_\text{eval}\). As a sample oracle we will combine all ite’s based on group \(\mathrm{g}\).

[18]:

df_post_treatment = df[df["t"] >= df["d"]]

df_post_treatment.groupby("d")["ite"].mean()

[18]:

d

2025-04-01 1.946044

2025-05-01 1.469743

2025-06-01 1.015535

Name: ite, dtype: float64

To obtain group-specific effects it is possible to aggregate several \(\widehat{ATT}(\mathrm{g},t_\text{pre},t_\text{eval})\) values based on the group \(\mathrm{g}\) by setting the aggregation="group" argument.

[19]:

aggregated_group = dml_obj.aggregate(aggregation="group")

print(aggregated_group)

_ = aggregated_group.plot_effects()

================== DoubleMLDIDAggregation Object ==================

Group Aggregation

------------------ Overall Aggregated Effects ------------------

coef std err t P>|t| 2.5 % 97.5 %

1.397243 0.104427 13.380082 0.0 1.19257 1.601916

------------------ Aggregated Effects ------------------

coef std err t P>|t| 2.5 % 97.5 %

2025-04 1.824981 0.182235 10.014424 0.0 1.467807 2.182156

2025-05 1.378262 0.114459 12.041502 0.0 1.153926 1.602598

2025-06 0.935033 0.101425 9.218968 0.0 0.736244 1.133822

------------------ Additional Information ------------------

Score function: observational

Control group: never_treated

Anticipation periods: 0

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/did/did_aggregation.py:368: UserWarning: Joint confidence intervals require bootstrapping which hasn't been performed yet. Automatically applying '.aggregated_frameworks.bootstrap(method="normal", n_rep_boot=500)' with default values. For different bootstrap settings, call bootstrap() explicitly before plotting.

warnings.warn(

The output is a DoubleMLDIDAggregation object which includes an overall aggregation summary based on group size.

Time Aggregation#

To obtain time-specific effects one can would like to average \(ATT(\mathrm{g}, t_\text{eval})\) over \(\mathrm{g}\) (respecting group size). As a sample oracle we will combine all ite’s based on group \(\mathrm{g}\). As oracle values, we obtain

[20]:

df_post_treatment.groupby("t")["ite"].mean()

[20]:

t

2025-04-01 0.962851

2025-05-01 1.510289

2025-06-01 1.991655

Name: ite, dtype: float64

To aggregate \(\widehat{ATT}(\mathrm{g},t_\text{pre},t_\text{eval})\), based on \(t_\text{eval}\), but weighted with respect to group size. Corresponds to Calendar Time Effects from the did-R-package.

For calendar time effects set aggregation="time".

[21]:

aggregated_time = dml_obj.aggregate("time")

print(aggregated_time)

fig, ax = aggregated_time.plot_effects()

================== DoubleMLDIDAggregation Object ==================

Time Aggregation

------------------ Overall Aggregated Effects ------------------

coef std err t P>|t| 2.5 % 97.5 %

1.40883 0.121677 11.578406 0.0 1.170347 1.647313

------------------ Aggregated Effects ------------------

coef std err t P>|t| 2.5 % 97.5 %

2025-04 0.987431 0.139868 7.059754 1.667999e-12 0.713296 1.261567

2025-05 1.387527 0.130302 10.648588 0.000000e+00 1.132141 1.642914

2025-06 1.851531 0.134213 13.795456 0.000000e+00 1.588479 2.114584

------------------ Additional Information ------------------

Score function: observational

Control group: never_treated

Anticipation periods: 0

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/did/did_aggregation.py:368: UserWarning: Joint confidence intervals require bootstrapping which hasn't been performed yet. Automatically applying '.aggregated_frameworks.bootstrap(method="normal", n_rep_boot=500)' with default values. For different bootstrap settings, call bootstrap() explicitly before plotting.

warnings.warn(

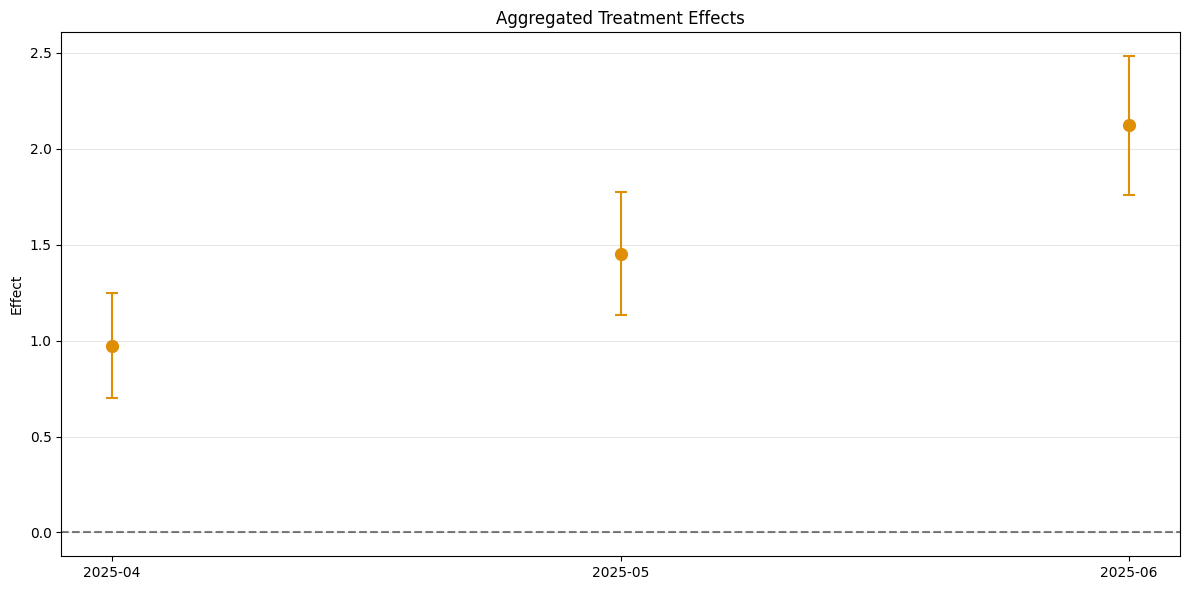

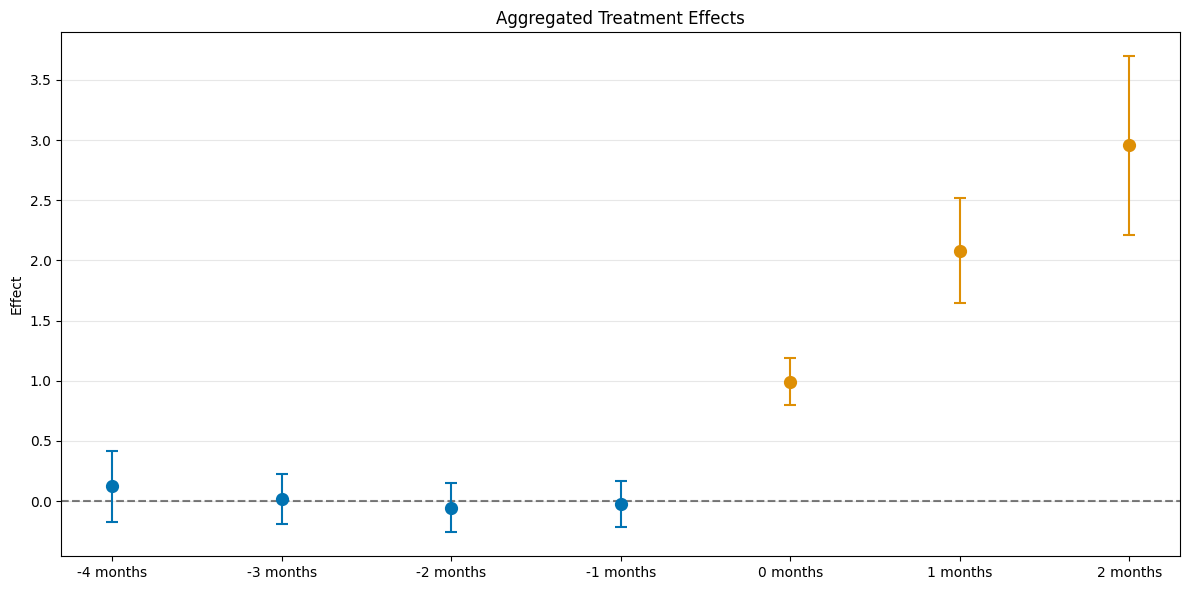

Event Study Aggregation#

To obtain event-study-type effects one can would like to aggregate \(ATT(\mathrm{g}, t_\text{eval})\) over \(e = t_\text{eval} - \mathrm{g}\) (respecting group size). As a sample oracle we will combine all ite’s based on group \(\mathrm{g}\). As oracle values, we obtain

[22]:

df["e"] = pd.to_datetime(df["t"]).values.astype("datetime64[M]") - \

pd.to_datetime(df["d"]).values.astype("datetime64[M]")

df.groupby("e")["ite"].mean()[1:]

[22]:

e

-122 days -0.018531

-92 days 0.030760

-61 days 0.032124

-31 days 0.003757

0 days 0.993790

31 days 1.948899

59 days 2.911880

Name: ite, dtype: float64

Analogously, aggregation="eventstudy" aggregates \(\widehat{ATT}(\mathrm{g},t_\text{pre},t_\text{eval})\) based on exposure time \(e = t_\text{eval} - \mathrm{g}\) (respecting group size).

[23]:

aggregated_eventstudy = dml_obj.aggregate("eventstudy")

print(aggregated_eventstudy)

aggregated_eventstudy.plot_effects()

================== DoubleMLDIDAggregation Object ==================

Event Study Aggregation

------------------ Overall Aggregated Effects ------------------

coef std err t P>|t| 2.5 % 97.5 %

1.826375 0.14807 12.334536 0.0 1.536163 2.116587

------------------ Aggregated Effects ------------------

coef std err t P>|t| 2.5 % 97.5 %

-4 months 0.109712 0.094031 1.166760 0.243307 -0.074586 0.294010

-3 months -0.012556 0.074036 -0.169597 0.865327 -0.157665 0.132552

-2 months -0.076871 0.068421 -1.123508 0.261222 -0.210973 0.057231

-1 months -0.038387 0.066848 -0.574249 0.565799 -0.169407 0.092632

0 months 0.983235 0.081288 12.095630 0.000000 0.823912 1.142557

1 months 1.721047 0.146992 11.708426 0.000000 1.432948 2.009147

2 months 2.774843 0.248031 11.187469 0.000000 2.288710 3.260975

------------------ Additional Information ------------------

Score function: observational

Control group: never_treated

Anticipation periods: 0

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/did/did_aggregation.py:368: UserWarning: Joint confidence intervals require bootstrapping which hasn't been performed yet. Automatically applying '.aggregated_frameworks.bootstrap(method="normal", n_rep_boot=500)' with default values. For different bootstrap settings, call bootstrap() explicitly before plotting.

warnings.warn(

[23]:

(<Figure size 1200x600 with 1 Axes>,

<Axes: title={'center': 'Aggregated Treatment Effects'}, ylabel='Effect'>)

Aggregation Details#

The DoubleMLDIDAggregation objects include several DoubleMLFrameworks which support methods like bootstrap() or confint(). Further, the weights can be accessed via the properties

overall_aggregation_weights: weights for the overall aggregationaggregation_weights: weights for the aggregation

To clarify, e.g. for the eventstudy aggregation

[24]:

print(aggregated_eventstudy)

================== DoubleMLDIDAggregation Object ==================

Event Study Aggregation

------------------ Overall Aggregated Effects ------------------

coef std err t P>|t| 2.5 % 97.5 %

1.826375 0.14807 12.334536 0.0 1.536163 2.116587

------------------ Aggregated Effects ------------------

coef std err t P>|t| 2.5 % 97.5 %

-4 months 0.109712 0.094031 1.166760 0.243307 -0.074586 0.294010

-3 months -0.012556 0.074036 -0.169597 0.865327 -0.157665 0.132552

-2 months -0.076871 0.068421 -1.123508 0.261222 -0.210973 0.057231

-1 months -0.038387 0.066848 -0.574249 0.565799 -0.169407 0.092632

0 months 0.983235 0.081288 12.095630 0.000000 0.823912 1.142557

1 months 1.721047 0.146992 11.708426 0.000000 1.432948 2.009147

2 months 2.774843 0.248031 11.187469 0.000000 2.288710 3.260975

------------------ Additional Information ------------------

Score function: observational

Control group: never_treated

Anticipation periods: 0

Here, the overall effect aggregation aggregates each effect with positive exposure

[25]:

print(aggregated_eventstudy.overall_aggregation_weights)

[0. 0. 0. 0. 0.33333333 0.33333333

0.33333333]

If one would like to consider how the aggregated effect with \(e=0\) is computed, one would have to look at the corresponding set of weights within the aggregation_weights property

[26]:

# the weights for e=0 correspond to the fifth element of the aggregation weights

aggregated_eventstudy.aggregation_weights[4]

[26]:

array([0. , 0. , 0.35864865, 0. , 0. ,

0. , 0. , 0. , 0.3227027 , 0. ,

0. , 0. , 0. , 0. , 0.31864865])

Taking a look at the original dml_obj, one can see that this combines the following estimates (only show month):

\(\widehat{ATT}(04,03,04)\)

\(\widehat{ATT}(05,04,05)\)

\(\widehat{ATT}(06,05,06)\)

[27]:

print(dml_obj.summary["coef"])

ATT(2025-04,2025-01,2025-02) 0.049358

ATT(2025-04,2025-02,2025-03) 0.010778

ATT(2025-04,2025-03,2025-04) 0.987431

ATT(2025-04,2025-03,2025-05) 1.712670

ATT(2025-04,2025-03,2025-06) 2.774843

ATT(2025-05,2025-01,2025-02) -0.025096

ATT(2025-05,2025-02,2025-03) -0.204573

ATT(2025-05,2025-03,2025-04) -0.123023

ATT(2025-05,2025-04,2025-05) 1.026166

ATT(2025-05,2025-04,2025-06) 1.730357

ATT(2025-06,2025-01,2025-02) 0.109712

ATT(2025-06,2025-02,2025-03) 0.000143

ATT(2025-06,2025-03,2025-04) -0.089618

ATT(2025-06,2025-04,2025-05) -0.008012

ATT(2025-06,2025-05,2025-06) 0.935033

Name: coef, dtype: float64

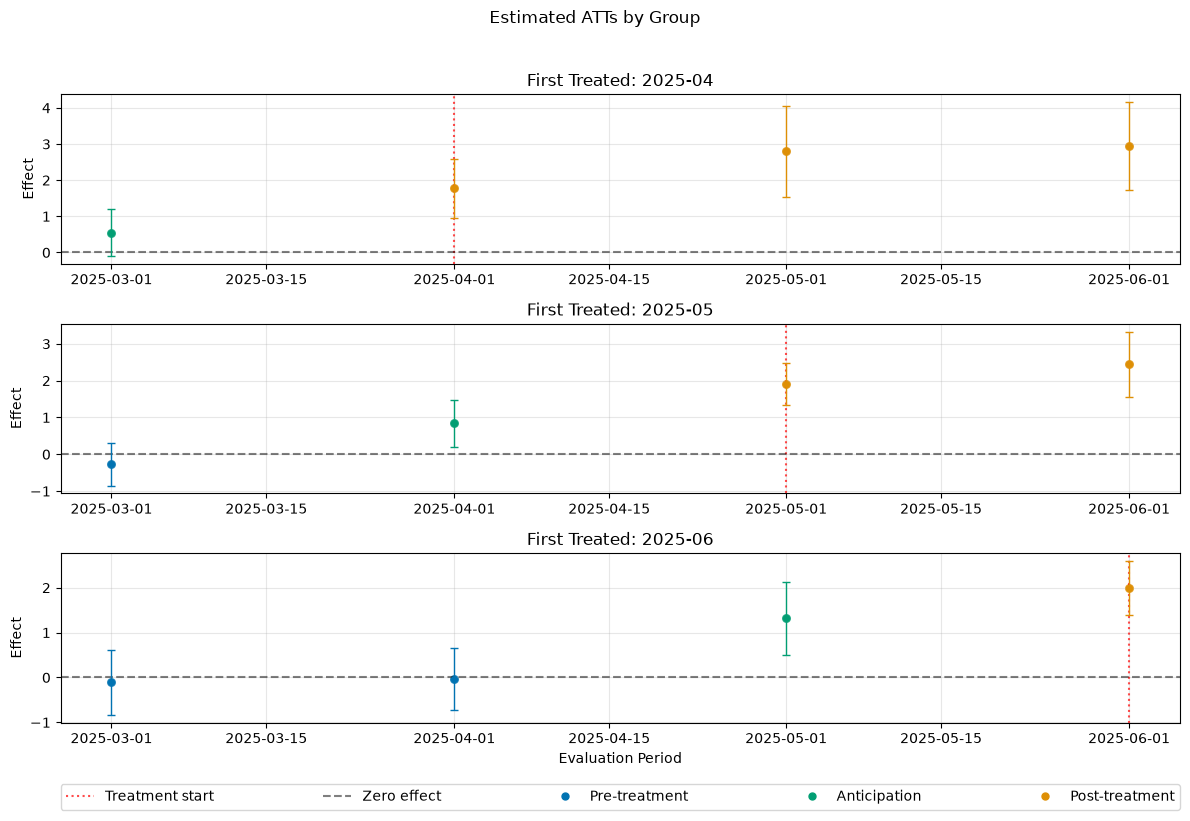

Anticipation#

As described in the Model Guide, one can include anticipation periods \(\delta>0\) by setting the anticipation_periods parameter.

Data with Anticipation#

The DGP allows to include anticipation periods via the anticipation_periods parameter. In this case the observations will be “shifted” such that units anticipate the effect earlier and the exposure effect is increased by the number of periods where the effect is anticipated.

[28]:

n_obs = 4000

n_periods = 6

df_anticipation = make_did_CS2021(n_obs, dgp_type=4, n_periods=n_periods, n_pre_treat_periods=3, time_type="datetime", anticipation_periods=1)

print(df_anticipation.shape)

df_anticipation.head()

(19242, 10)

[28]:

| id | y | y0 | y1 | d | t | Z1 | Z2 | Z3 | Z4 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 0 | 206.331313 | 206.331313 | 205.264263 | 2025-06-01 | 2025-01-01 | -0.380002 | -1.130733 | 0.08537 | -0.358659 |

| 2 | 0 | 206.201148 | 206.201148 | 205.110981 | 2025-06-01 | 2025-02-01 | -0.380002 | -1.130733 | 0.08537 | -0.358659 |

| 3 | 0 | 203.343582 | 203.343582 | 200.592336 | 2025-06-01 | 2025-03-01 | -0.380002 | -1.130733 | 0.08537 | -0.358659 |

| 4 | 0 | 201.128249 | 201.128249 | 200.150311 | 2025-06-01 | 2025-04-01 | -0.380002 | -1.130733 | 0.08537 | -0.358659 |

| 5 | 0 | 197.306384 | 200.026015 | 197.306384 | 2025-06-01 | 2025-05-01 | -0.380002 | -1.130733 | 0.08537 | -0.358659 |

To visualize the anticipation, we will again plot the “oracle” values

[29]:

df_anticipation["ite"] = df_anticipation["y1"] - df_anticipation["y0"]

df_anticipation["First Treated"] = df_anticipation["d"].dt.strftime("%Y-%m").fillna("Never Treated")

agg_df_anticipation = df_anticipation.groupby(["t", "First Treated"]).agg(**agg_dictionary).reset_index()

agg_df_anticipation.head()

[29]:

| t | First Treated | y_mean | y_lower_quantile | y_upper_quantile | ite_mean | ite_lower_quantile | ite_upper_quantile | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2025-01-01 | 2025-04 | 208.935423 | 191.733809 | 225.465295 | 0.047747 | -2.120268 | 2.415732 |

| 1 | 2025-01-01 | 2025-05 | 211.087262 | 194.180903 | 228.262456 | 0.013682 | -2.413062 | 2.340068 |

| 2 | 2025-01-01 | 2025-06 | 212.884695 | 196.325313 | 229.635862 | -0.015537 | -2.392026 | 2.339877 |

| 3 | 2025-01-01 | Never Treated | 217.330308 | 200.943817 | 234.090039 | 0.083961 | -2.234492 | 2.438055 |

| 4 | 2025-02-01 | 2025-04 | 208.993808 | 183.524228 | 233.394549 | 0.021260 | -2.215118 | 2.302010 |

One can see that the effect is already anticipated one period before the actual treatment assignment.

[30]:

plot_data(agg_df_anticipation, col_name='ite')

Initialize a corresponding DoubleMLPanelData object.

[31]:

dml_data_anticipation = DoubleMLPanelData(

data=df_anticipation,

y_col="y",

d_cols="d",

id_col="id",

t_col="t",

x_cols=["Z1", "Z2", "Z3", "Z4"],

datetime_unit="M"

)

ATT Estimation#

Let us take a look at the estimation without anticipation.

[32]:

dml_obj_anticipation = DoubleMLDIDMulti(dml_data_anticipation, **default_args)

dml_obj_anticipation.fit()

dml_obj_anticipation.bootstrap(n_rep_boot=5000)

dml_obj_anticipation.plot_effects()

[32]:

(<Figure size 1200x800 with 4 Axes>,

[<Axes: title={'center': 'First Treated: 2025-04'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-05'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-06'}, xlabel='Evaluation Period', ylabel='Effect'>])

The effects are obviously biased. To include anticipation periods, one can adjust the anticipation_periods parameter. Correspondingly, the outcome regression (and not yet treated units) are adjusted.

[33]:

dml_obj_anticipation = DoubleMLDIDMulti(dml_data_anticipation, **(default_args| {"anticipation_periods": 1}))

dml_obj_anticipation.fit()

dml_obj_anticipation.bootstrap(n_rep_boot=5000)

dml_obj_anticipation.plot_effects()

[33]:

(<Figure size 1200x800 with 4 Axes>,

[<Axes: title={'center': 'First Treated: 2025-04'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-05'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-06'}, xlabel='Evaluation Period', ylabel='Effect'>])

Group-Time Combinations#

The default option gt_combinations="standard" includes all group time values with the specific choice of \(t_\text{pre} = \min(\mathrm{g}, t_\text{eval}) - 1\) (without anticipation) which is the weakest possible parallel trend assumption.

Other options are possible or only specific combinations of \((\mathrm{g},t_\text{pre},t_\text{eval})\).

All Combinations#

The option gt_combinations="all" includes all relevant group time values with \(t_\text{pre} < \min(\mathrm{g}, t_\text{eval})\), including longer parallel trend assumptions. This can result in multiple estimates for the same \(ATT(\mathrm{g},t)\), which have slightly different assumptions (length of parallel trends).

[34]:

dml_obj_all = DoubleMLDIDMulti(dml_data, **(default_args| {"gt_combinations": "all"}))

dml_obj_all.fit()

dml_obj_all.bootstrap(n_rep_boot=5000)

dml_obj_all.plot_effects()

[34]:

(<Figure size 1200x800 with 4 Axes>,

[<Axes: title={'center': 'First Treated: 2025-04'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-05'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-06'}, xlabel='Evaluation Period', ylabel='Effect'>])

Universal Base Period#

The option gt_combinations="universal" set \(t_\text{pre} = \mathrm{g} - \delta - 1\), corresponding to a universal/constant comparison or base period.

Remark that this implies \(t_\text{pre} > t_\text{eval}\) for all pre-treatment periods (accounting for anticipation). Therefore these effects do not have the same straightforward interpretation as ATT’s.

[35]:

dml_obj_universal = DoubleMLDIDMulti(dml_data, **(default_args| {"gt_combinations": "universal"}))

dml_obj_universal.fit()

dml_obj_universal.bootstrap(n_rep_boot=5000)

dml_obj_universal.plot_effects()

[35]:

(<Figure size 1200x800 with 4 Axes>,

[<Axes: title={'center': 'First Treated: 2025-04'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-05'}, ylabel='Effect'>,

<Axes: title={'center': 'First Treated: 2025-06'}, xlabel='Evaluation Period', ylabel='Effect'>])

Selected Combinations#

Instead it is also possible to just submit a list of tuples containing \((\mathrm{g}, t_\text{pre}, t_\text{eval})\) combinations. E.g. only two combinations

[36]:

gt_dict = {

"gt_combinations": [

(np.datetime64('2025-04'),

np.datetime64('2025-01'),

np.datetime64('2025-02')),

(np.datetime64('2025-04'),

np.datetime64('2025-02'),

np.datetime64('2025-03')),

]

}

dml_obj_all = DoubleMLDIDMulti(dml_data, **(default_args| gt_dict))

dml_obj_all.fit()

dml_obj_all.bootstrap(n_rep_boot=5000)

dml_obj_all.plot_effects()

[36]:

(<Figure size 1200x800 with 2 Axes>,

[<Axes: title={'center': 'First Treated: 2025-04'}, xlabel='Evaluation Period', ylabel='Effect'>])