Note

-

Download Jupyter notebook:

https://docs.doubleml.org/stable/examples/py_double_ml_robust_iv.ipynb.

Python: Confidence Intervals for Instrumental Variables Models That Are Robust to Weak Instruments#

In this example we will show how to use the DoubleML package to obtain confidence sets for the treatment effects that are robust to weak instruments. Weak instruments are those that have a relatively weak correlation with the treatment. It is well known that in this case, standard methods to construct confidence intervals have poor properties and can have coverage much lower than the nominal value. We will assume that the reader of this notebook is already familiar with DoubleML and how it can be used to fit instrumental variable models.

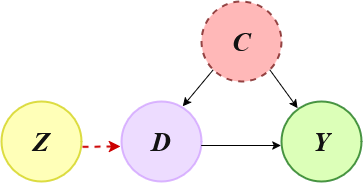

Throughout this example

\(Z\) is the instrument,

\(X\) is a vector of covariates,

\(D\) is treatment variable,

\(Y\) is the outcome.

Next, we will run a simulation, where we will generate two synthetic data sets, one where the instrument is weak and another where it is not. Then, we will compare the output of the standard way to compute confidence intervals using the DoubleMLIIVM class, with the confidence sets computed using the robust_confset() method from the same class. We will see that using the robust_confset() method is an easy way to ensure the results of an analysis are robust to weak instruments.

[1]:

import numpy as np

import pandas as pd

import random

from sklearn.base import BaseEstimator, ClassifierMixin

from sklearn.linear_model import LinearRegression, LogisticRegression

import doubleml as dml

np.random.seed(1234)

random.seed(1234)

Running a small simulation#

The following function generates data from an instrumental variables model. The true_effect argument is the estimand of interest, the true effect of the treatment on the outcome. The instrument_strength argument is a measure of the strength of the instrument. The higher it is, the stronger the correlation is between the instrument and the treatment. Notice that the instrument is fully randomized.

[2]:

def generate_weakiv_data(n_samples, true_effect, instrument_strength):

u = np.random.normal(0, 2, size=n_samples)

X = np.random.normal(0, 1, size=n_samples)

Z = np.random.binomial(1, 0.5, size=n_samples)

D = instrument_strength * Z + u

D = np.array(D > 0, dtype=int)

Y = true_effect * D + np.sign(u)

return pd.DataFrame({"Y": Y, "Z": Z, "D": D, "X": X})

To fit the DML model, we need to decide on how we will estimate the nuisance functions. We will use a linear regression model for \(g\), and a logistic regression for \(r\). We will assume that we know the true \(m\) function, as is the case in a controlled experiment, such as an AB test. The following class defines defines this “fake” estimator.

[3]:

class TrueMFunction(BaseEstimator, ClassifierMixin):

def __init__(self, prob_dist=(0.5, 0.5)):

self.prob_dist = prob_dist

def fit(self, X, y):

self.prob_dist_ = np.array(self.prob_dist)

self.classes_ = np.array(sorted(set(y)))

return self

def predict_proba(self, X):

return np.tile(self.prob_dist_, (len(X), 1))

def predict(self, X):

return np.full(len(X), self.classes_[np.argmax(self.prob_dist_)])

We will now run a loop, where for each of \(100\) replications we will generate data using the previously defined function. We will take a sample size of \(5000\), a true effect equal to \(1\), and take two possible values for the instrument strength: \(0.003\) and \(1\). In the latter case the instrument is strong, in the former it is weak. We will then compute both the robust and the standard confidence intervals, check whether they contain the true effect, and compute their length.

[4]:

n_samples = 5000

true_effect = 1

output_list = []

for _ in range(100):

for instrument_strength in [0.003, 1]:

dataset = generate_weakiv_data(n_samples = n_samples, true_effect = true_effect, instrument_strength = instrument_strength)

dml_data = dml.DoubleMLData(

dataset, y_col='Y', d_cols='D',

z_cols='Z', x_cols='X'

)

ml_g = LinearRegression()

ml_m = TrueMFunction()

ml_r = LogisticRegression(penalty=None)

dml_iivm = dml.DoubleMLIIVM(dml_data, ml_g, ml_m, ml_r)

dml_iivm.fit()

dml_standard_ci = dml_iivm.confint(joint=False)

dml_robust_confset = dml_iivm.robust_confset()

dml_covers = dml_standard_ci["2.5 %"].iloc[0] <= true_effect <= dml_standard_ci["97.5 %"].iloc[0]

robust_covers = any(interval[0] <= true_effect <= interval[1] for interval in dml_robust_confset)

dml_length = dml_standard_ci["97.5 %"].iloc[0] - dml_standard_ci["2.5 %"].iloc[0]

dml_robust_length = max(interval[1] - interval[0] for interval in dml_robust_confset)

output_list.append({

"instrument_strength": instrument_strength,

"dml_covers": dml_covers,

"robust_covers": robust_covers,

"dml_length": dml_length,

"robust_length": dml_robust_length

})

results_df = pd.DataFrame(output_list)

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1232: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) neither a regressor nor a classifier. Method predict is used for prediction.

warnings.warn(

/home/runner/work/doubleml-docs/doubleml-docs/doubleml-for-py/doubleml/double_ml.py:1240: UserWarning: Learner provided for ml_m is probably invalid: TrueMFunction() is (probably) no classifier.

warnings.warn(warn_msg_prefix + f"{str(learner)} is (probably) no classifier.")

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(

/opt/hostedtoolcache/Python/3.12.13/x64/lib/python3.12/site-packages/sklearn/linear_model/_logistic.py:451: OptimizeWarning: Unknown solver options: iprint

opt_res = optimize.minimize(